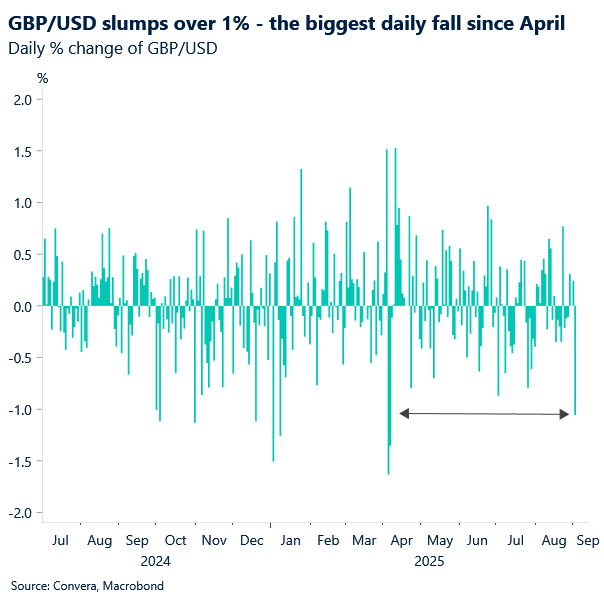

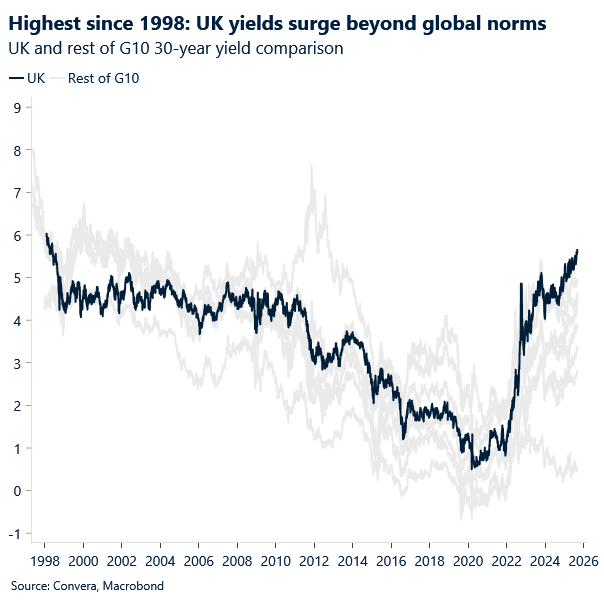

Sterling sentiment snaps as bond turmoil bites

Bond market stress is once again haunting the pound despite the lack of dysfunctional moves. indeed, the issue is global in nature too. Long-end yields are rising across major economies, curves are steepening, and investor anxiety over sovereign debt and inflation is intensifying. But while UK 30-year gilt yields didn’t move dramatically yesterday, they’ve quietly reached levels last seen in 1998 – a milestone that’s hard to ignore.

Sterling’s sensitivity to rising yields is striking as it is underperforms across the G10, with GBP/USD suffering its steepest one-day drop since April, when Liberation Day headlines triggered a broad risk-off move. The pair has broken below $1.34, with limited support until $1.32, while GBP/EUR has slipped back under €1.15, leaving it nearly 5% lower year-to-date.

Markets don’t always react to new information – they move when old risks become impossible to ignore. We’ve long warned that the UK’s stagflation backdrop and the Bank of England’s (BoE) hawkish stance meant sterling’s gains were resting on shaky foundations. Now, fiscal concerns are taking centre stage.

The government’s estimated £51 billion fiscal gap is fuelling investor unease. Chancellor Rachel Reeves faces a tough balancing act: finding savings amid internal party tensions and likely needing to raise taxes again in the autumn budget. These concerns are driving long-end yields higher and amplifying sterling’s fragility.

There may be some relief later this month. The BoE’s September 18 policy meeting is expected to include a review of its bond-selling pace. Governor Andrew Bailey has previously flagged concerns about illiquidity and curve steepening, suggesting the central bank may slow its quantitative tightening – particularly at the long end.

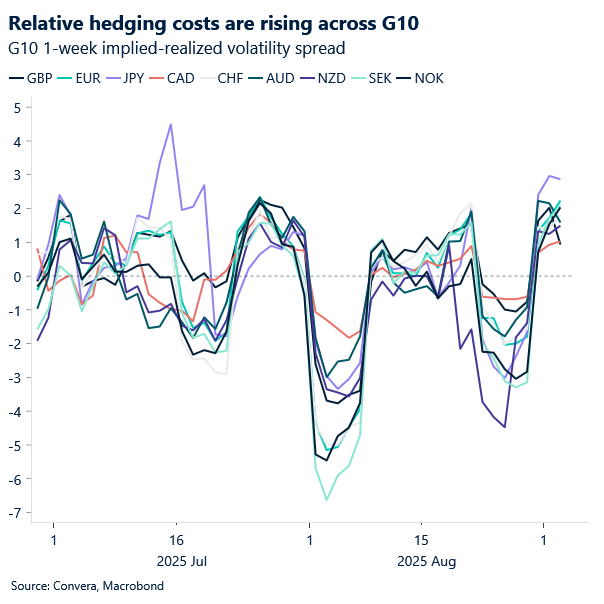

Still, the UK remains at the epicentre of global bond stress and in the FX options market, the volatility skew is flattening, signalling traders are pricing in further near-term downside. Elevated realised volatility is keeping hedging costs high, reinforcing the cautious tone around GBP.

‘Fortress North America’: Mexico’s balancing act

Mexico’s recent imposition of tariffs on imported footwear, a measure particularly aimed at curbing Chinese products, highlights a significant shift in its trade policy. The move, banning temporary imports under the IMMEX program and requiring a 25% tariff, is a direct response to the decimation of its domestic footwear industry. Mexican officials report a catastrophic impact from cheap, often-copied, Asian imports, which have undercut local manufacturers, leading to a sharp decline in GDP, production, and employment within the sector. While framed as a protectionist measure for local industries, this action also signals a growing alignment with the United States’ strategy to limit Chinese imports into North America.

This strategic alignment is even more pronounced in the highly contentious automotive sector. The United States has expressed significant concern that Chinese automakers are using Mexico as a backdoor to circumvent U.S. tariffs by establishing assembly plants. While Mexico seeks to attract foreign direct investment and create jobs, it is simultaneously under pressure to prevent Chinese-made vehicles from flooding the U.S. market under the preferential terms of the USMCA. The U.S. leverage is significant, and Mexico is walking a fine line, reportedly curbing some incentives for Chinese auto firms to avoid jeopardizing its crucial trade relationship with its northern neighbor.

The broader context for these actions is the upcoming 2026 review of the USMCA/CUSMA trade deal. The agreement’s mandatory review provides the U.S. with a powerful tool to pressure Mexico on various trade issues, including the flow of Chinese goods. By implementing its own protectionist measures and appearing to take a more proactive stance against “unfair” Chinese competition, Mexico is effectively signaling its commitment to a shared North American trade agenda. This proactive approach could be a strategic move to secure a more favorable position in the renegotiations, demonstrating to the U.S. that Mexico is a reliable partner in the creation of a more secure and integrated North American trade bloc, a vision some U.S. officials have termed “Fortress North America.”

In essence, Mexico is navigating a complex geopolitical and economic landscape. The tariffs on footwear are not an isolated event but rather part of a larger trend where Mexico is re-evaluating its trade relationships and policies. While domestic industrial protection is the stated goal, the subtext is a strategic effort to appease the United States and preemptively address concerns ahead of the USMCA’s review. This balancing act shows Mexico’s priority of maintaining its critical trade ties with the U.S., even if it means adopting policies that are a significant departure from its previous free-trade orientation.

Summer’s lull looks over

Volatility is back, and this time it’s not driven by fresh headlines but by a long-simmering repricing of risk. Global long-end yields are grinding higher, yield curves are steepening, and investors are finally confronting the structural threats – fiscal fragility, inflation persistence, and policy uncertainty – that have been building for months.

The shift in tone is partly seasonal. With summer behind us and institutional desks fully staffed, liquidity has returned – and so has price sensitivity. What was tolerated in August is now triggering defensive repositioning across asset classes. FX options markets are flashing caution, with demand rising for downside protection and hedging costs staying elevated.

The dollar’s recent bounce looks more like a reflection of fragility elsewhere than a confident bid for safety though. The Japanese yen, for instance, remains weighed down by domestic political noise, and gold has lost momentum despite its record highs. We doubt the dollar’s rebound has legs in it unless backed by a more supportive US economic backdrop.

On the data front, the ISM manufacturing survey offered a mixed picture: new orders showed signs of life, but employment remains worryingly soft. If these trends persist, the Fed may have room to ease, but global crosscurrents could blunt the impact.

Today’s US JOLTS report will be closely watched. Job openings are expected to have dipped slightly in July to around 7.37 million. But even at these levels, demand for labor remains well above the pre-pandemic average of 7 million seen in 2018–19 – raising fresh concerns about labor market tightness and its implications for wage inflation and Fed policy.

All eyes are also on Friday’s payrolls report. A weak print would reinforce rate cut expectations, while a hold risks reigniting political pressure on the Fed, adding another layer of uncertainty to an already fragile macro backdrop.

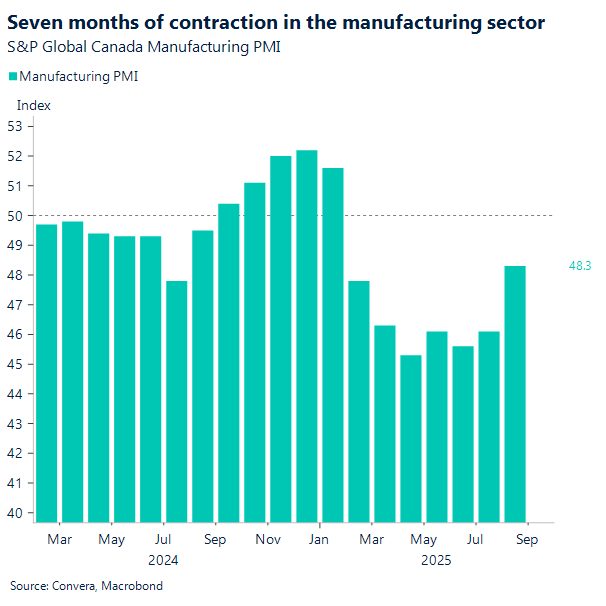

Manufacturing struggles amidst trade tensions

The Canadian manufacturing sector continues to face significant headwinds, primarily driven by the prolonged trade dispute with the United States. While the latest PMI data from August 2025 showed a slight easing in the pace of contraction, the sector remains in a state of decline, marked by seven consecutive months of shrinking activity. This sustained downturn is a direct consequence of U.S. tariffs, which have severely impacted demand from the largest export market and disrupted vital supply chains. The resulting decline in new orders and output has forced manufacturers to continue reducing their workforce, leading to the seventh consecutive month of job losses.

The report reveals a complex and uncertain outlook. Manufacturers are grappling with the dual pressure of lower demand and elevated input costs, which rose to a three-month high even as the sector contracts. This difficult environment is further complicated by the trade policy uncertainty, making it difficult for firms to plan and invest for the future. Although business confidence saw a modest improvement, it remains well below historical levels. The deep integration of the Canadian and U.S. economies leaves the manufacturing sector particularly vulnerable to these trade disruptions.

Starting the month, the Canadian dollar has been trading between 1.381 and 1.373. A sell-off in long-term bond markets has made headlines and spread to other markets, with the VIX spiking on fears of stagflation in major economies. The U.S. dollar found some support at the start of the week due to stress in the U.K. bond market and Chinese authorities setting the USD/CNY exchange rate slightly higher. However, the overall bias remains negative for the dollar this week, as markets anticipate another downward revision to Friday’s job report, continuing the trend from the last few months.

CAD recovers against the Pound

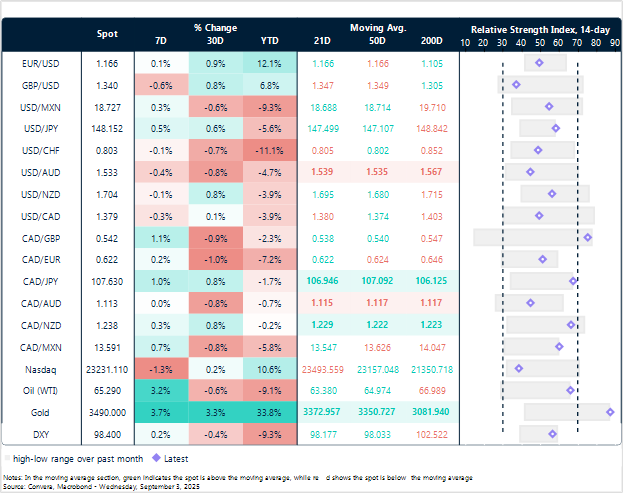

Table: Currency trends, trading ranges and technical indicators

Key global risk events

Calendar: September 1-5

All times are in EST.

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.