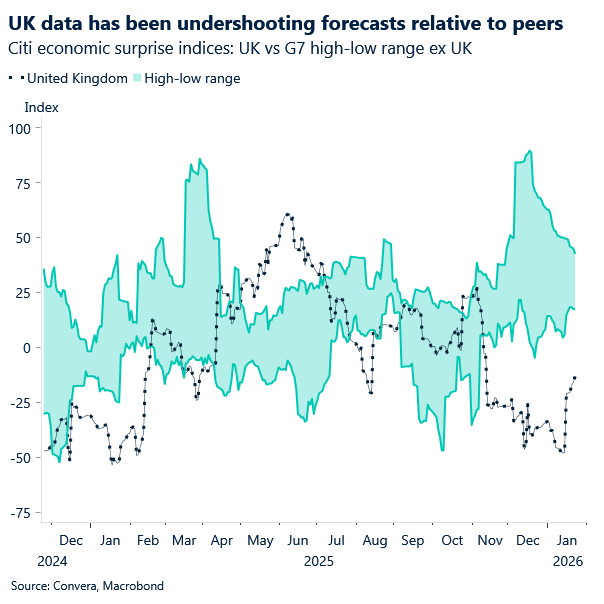

GBP: Green shoots break through UK gloom

The UK economic backdrop has made grim reading for much of the past six months. The economic surprise index sinking toward –50 underlines how consistently data has undershot expectations — from sluggish activity to softer labour‑market momentum and fading inflation pressures. It’s a signal not just of weak outcomes, but of an economy repeatedly disappointing even the already‑downgraded forecasts that preceded them.

But the latest releases hint that the tide may be turning. Retail sales beat expectations in December, rising 0.4% including fuel and 0.3% excluding it, defying predictions for a flat print. Today’s GfK survey also showed a modest improvement in consumer confidence, suggesting households may finally be regaining some footing after a bruising year.

It’s far too early to declare a UK rebound, but the data is no longer one‑way traffic. After months of disappointment, even small upside surprises matter — especially with inflation cooling and rate cuts approaching. If these green shoots broaden into Q2, the UK could shift from “perennial laggard” to “undervalued recovery story,” offering a more supportive backdrop for sterling and domestic assets than markets currently assume.

Sterling has spent the week caught between global risk swings and shifting dollar sentiment, with geopolitics briefly flipping the greenback from cyclical bull to something closer to a structural bear and pulling $1.35 into view. But with focus turning back to fundamentals, if UK unemployment stabilises, inflation returns to 2%, and the BoE continues easing, relative growth dynamics could turn more sterling‑friendly — even if the UK’s yield appeal remains softer.

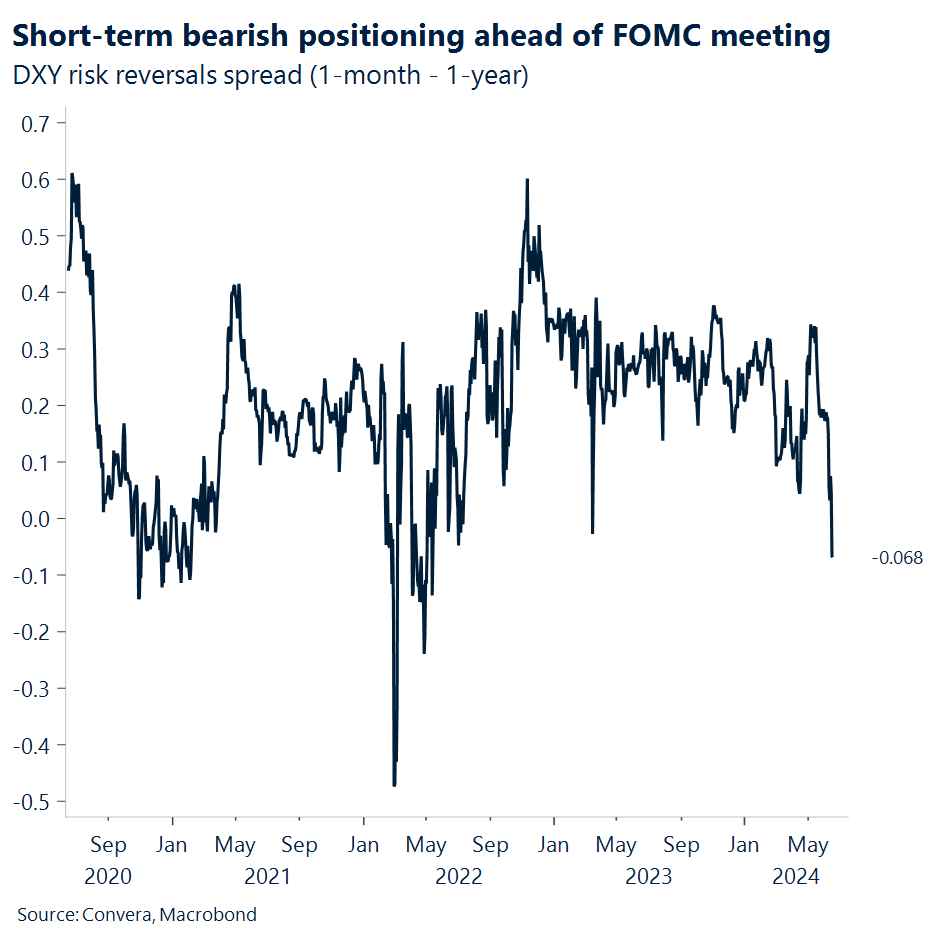

USD: Positioning into the FOMC

The latest US macro data and yesterday’s price action are telling different stories, and the tension looks tactical rather than structural. On the data side, the Bureau of Economic Analysis revised Q3‑2025 real GDP up to 4.4% SAAR, underscoring a still‑resilient US expansion as we head into 2026. On the tape yesterday, the dollar was broadly softer by roughly 0.4%, including declines against the euro and the pound even as equity volatility eases with the VIX drifting toward the mid‑teens. That combination, USD drifting lower with calmer risk, suggests position‑squaring into next week’s Fed rather than a fresh macro regime.

Under the surface, the GDP detail reinforces the idea that private‑sector momentum remains the main engine. On BEA’s industry contribution tables for Q3‑2025, Information, Finance & Insurance, and Professional, Scientific & Technical Services together contributed about 1.6 percentage points to the quarter’s growth, while Durable Goods Manufacturing added ~0.5 pp; by contrast, Federal government subtracted ~0.04 pp. Importantly, while the autumn government shutdown disrupted publication schedules and forced BEA to consolidate estimates, the agency does not attribute the government value‑added decline to the shutdown itself, so maybe this is a data‑release issue than a growth‑driver.

The market, however, is focused on the near‑term policy event risk. The FOMC meets Jan 27–28, with the decision and Chair’s press conference slated for next Wednesday. With the federal funds target range at 3.50%–3.75% and the effective rate near 3.64%, traders appear to be trimming longs and leaning on technicals rather than making a high‑conviction macro call a week early. The result is a softer USD alongside lower equity vol, which is exactly what you would expect in a pre‑event, low‑visibility window, especially after a run of firm US growth prints.

Set against the global backdrop, the case for a durable, fundamental USD down‑trend is still weak without new information. The euro area grew 0.3% q/q in Q3‑2025 (≈1.2% annualized), far from a boom, while the US 10‑year has spent much of January cycling in the ~4.15%–4.30% zone, hardly a backdrop that screams “aggressive Fed cutting cycle.”

The fiscal/policy backdrop adds another layer. Late‑2025 legislation extended and expanded elements of the 2017 tax law (for example, rate schedules and the standard deduction) and adjusted the SALT cap structure for a period, changes that could support disposable income and consumption in 2026, with obvious caveats around implementation and behavior. If those enacted changes do provide a modest tailwind, they reinforce the notion that the US remains growth‑resilient relative to many developed peers heading into mid‑year, again complicating the case for an extended USD downswing absent a bond‑market or policy‑guidance shock.

Pulling it together, yesterday’s USD softness looks like tactical de‑risking and re‑positioning into the Jan 27–28 FOMC, not a referendum on US macro. The data still show a private‑sector‑led expansion with Q3 GDP at 4.4% SAAR; the global dispersion in growth and policy rates still argues for US yields holding a relative premium; and market volatility remains subdued. If the Fed’s tone next Wednesday reiterates that cuts are data‑dependent and the bond market keeps the 10‑year anchored near 4.2%, the fundamental current will continue to run against momentum‑driven USD shorts. In that setup, reversal risk is elevated: bears leaning on the calm may find themselves caught wrong‑footed if the policy path or term premium is repriced even modestly.

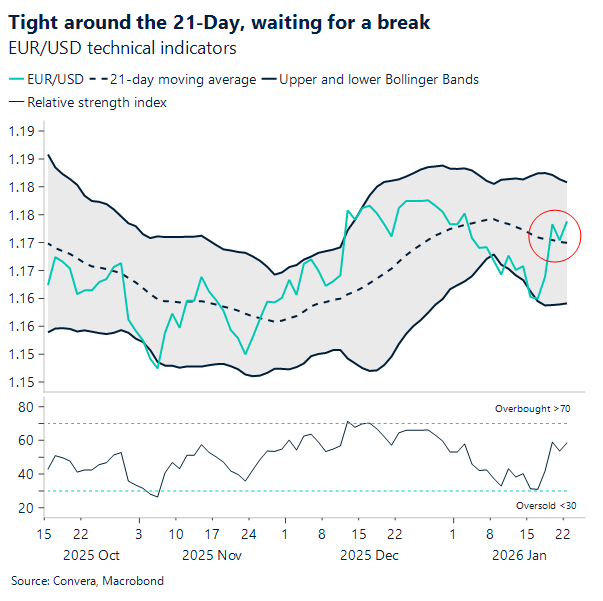

EUR: Still no break from 1.17

Yesterday the US dollar was broadly offered as markets continued to digest incoming geopolitical developments. EUR/USD remains reluctant to move away from the 1.17 zone, having re-explored it yesterday after finding clear support at the 50‑day moving average near 1.1670. With uncertainty still surrounding events in Greenland, technicals may dominate in the near term before the US-led macro narrative takes clearer shape next week (FOMC policy meeting). 1.1760 capped the upside yesterday. After this week’s mean‑reversion back toward the 21‑day moving average, the line remains the key pivot, making today’s close a clearer test of whether bulls still hold the advantage. A close below the average would simply fold back into the prevailing mean‑reversion pattern.

Key US data releases confirmed solid GDP growth and stable labour‑market conditions, setting the stage for what we expect will be a more confident assessment of the US economy at next week’s Fed meeting on the 28th. This should limit any further testing of the 1.17 zone. We continue to favour a move lower toward 1.16 in the coming days. Meanwhile, the ECB’s December meeting minutes showed a highly divided Governing Council on the inflation outlook, with some members focused on downside risks and others on upside threats. The path ahead will depend on incoming data and shifts in ECB communication, but for now the stance remains neutral at 2%.

For today, keep an eye out for a slate of preliminary PMI readings across several eurozone economies.

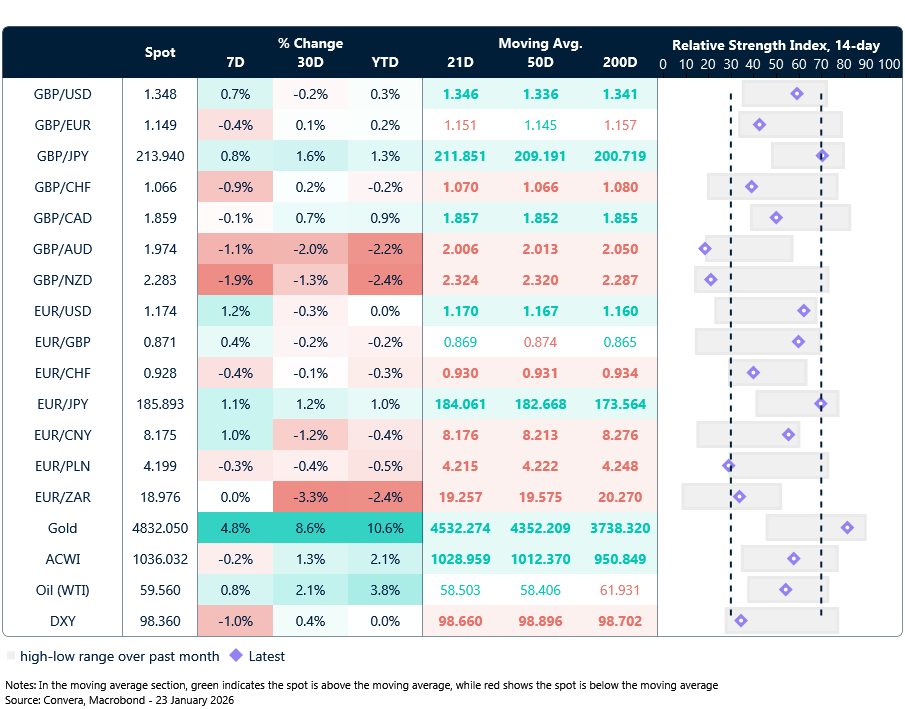

Market snapshot

Table: Currency trends, trading ranges & technical indicators

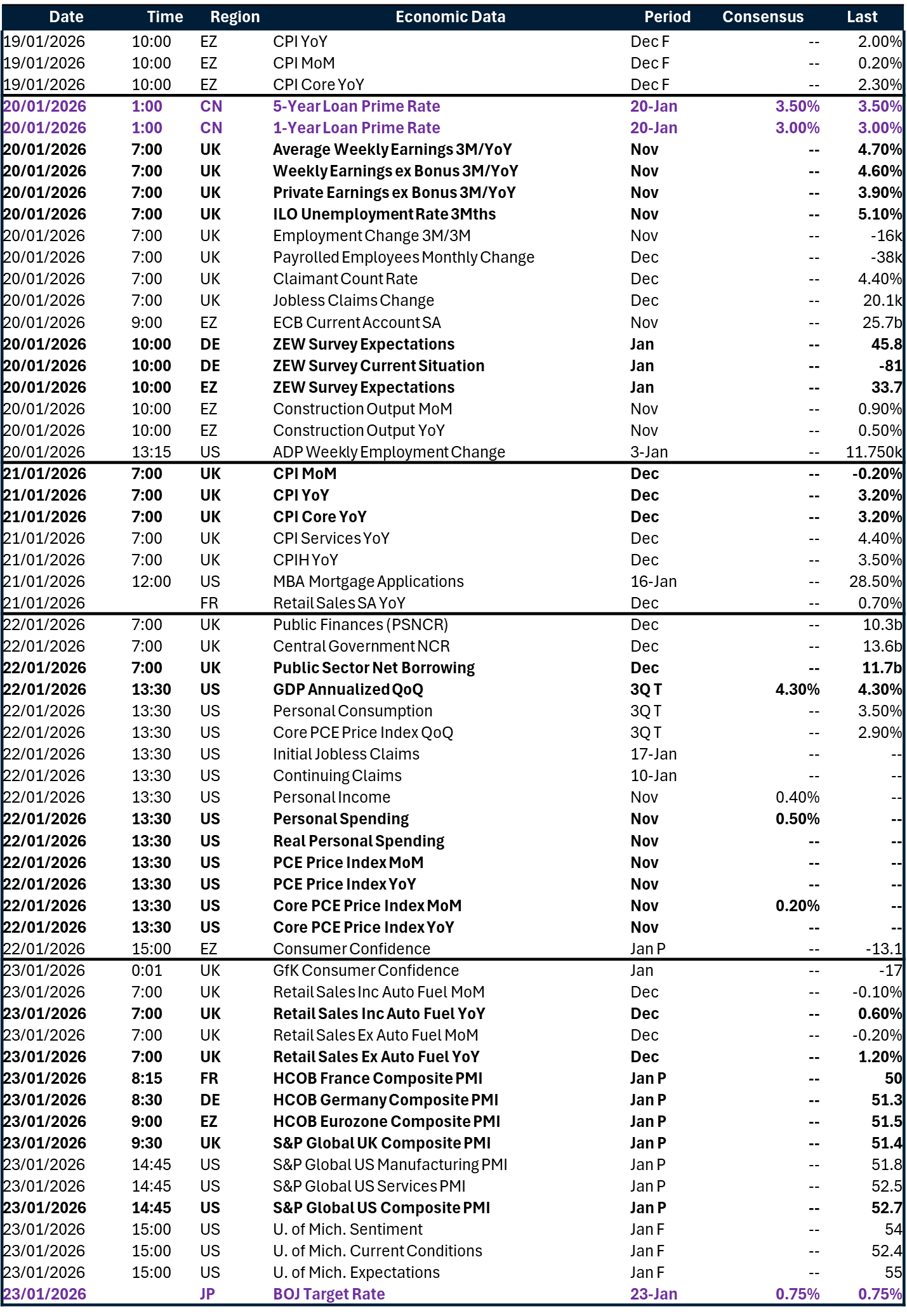

Key global risk events

Calendar: January 19-23

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.