USD: Conflicting cues limit USD momentum

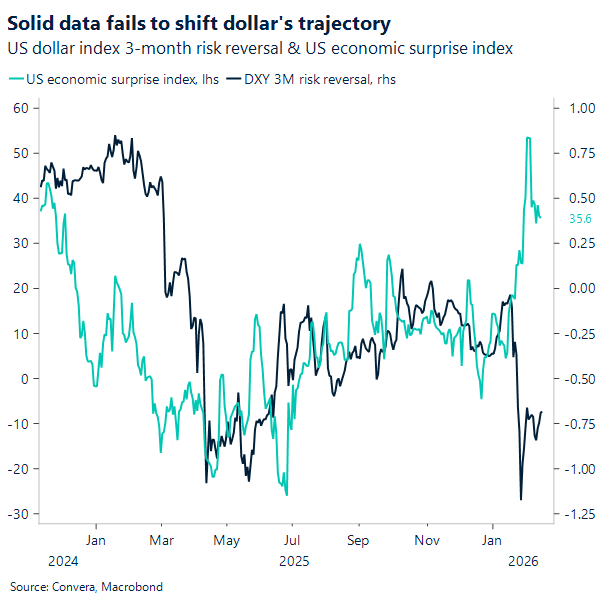

The US dollar index ended last week in the red after a choppy stretch dominated by AI‑driven equity jitters and mixed macro signals for Fed policy. It seems markets are biased to trade weak or dovish US data, with investors increasingly convinced the Fed will respond asymmetrically to any signs of softness.

Take the stronger‑than‑expected jobs report earlier last week: it failed to give the dollar any lasting lift. Downward revisions to 2025 employment and unusually concentrated sectoral hiring diluted the headline beat. But at the same time, the build‑up in US‑specific risk premia, tied to concerns over policy credibility, has overshadowed any USD‑positive impulse too. The recent AI‑led equity correction hasn’t changed that dynamic; its US‑centric nature has largely offset any unwind of residual dollar shorts. This also speaks to the dollar’s waning safe haven appeal during times of global market unease.

Then there’s the inflation story. On Friday, the cooler-than-expected monthly change in the CPI rate for January saw traders ramp up Fed easing bets, but the details were less reassuring. The downside surprise was driven mainly by energy, a move unlikely to persist given the rebound in oil prices. Core inflation was broadly in line — arguably firmer than feared — with core services posting their largest monthly rise in a year, suggesting price pressures are not yet on a sustainably lower trajectory.

Even so, Fed funds futures continue to price a meaningful easing cycle, with markets assigning a rising probability to three cuts this year — July, October and potentially December. As a result, nominal rate differentials are set to narrow against the dollar, particularly versus the yen, AUD and NZD.

This week, the FOMC Minutes (Wed) and the PCE inflation release (Fri) are the key events to watch.

GBP: Sterling steadies as politics recede

Sterling enters the week with its political risk premium having eased, after last week’s chorus of UK cabinet ministers publicly backed Prime Minister Keir Starmer following weeks of backlash from key Labour Party members urging him to step down.

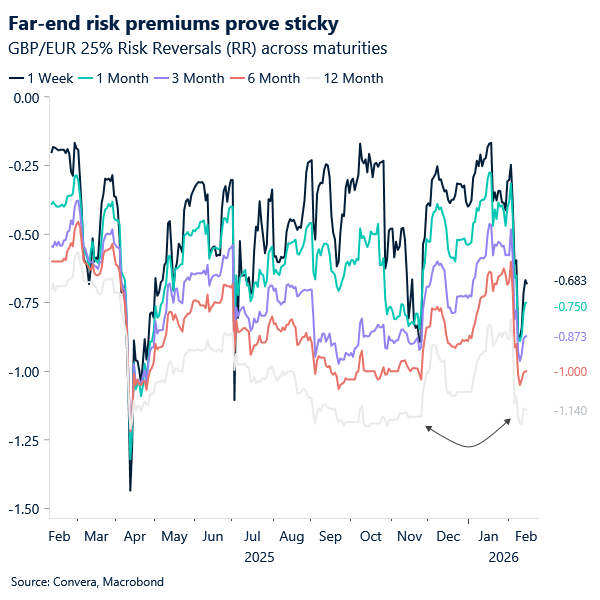

That said, when observing GBP/EUR risk reversals across tenors – a measure of sentiment – the curve appears to have improved more sharply at the short end, signalling that investors still expect further political flareups but are now more inclined to hedge against GBP weakness further out. In plain words, investors see political risk as having receded, but far from disappeared.

From a technical perspective, the stance is supported: GBP/EUR continues to hold above the 100‑day moving average near 1.1459, a level that has acted as reliable support since December, and now appears to be re‑establishing itself above the 50‑day too (1.1492). Overall, the resilience of spot suggests that the heavier pressure is still being expressed through options rather than outright selling, with investors likely waiting for clearer catalysts before committing to more directional moves. This month’s by‑election and the run‑up to May’s state election remain the key domestic risk events on the horizon.

On the macro side, the focus this week is squarely on UK inflation. The BoE’s dovish tilt hinges almost entirely on the disinflationary trajectory, and with headline CPI still at 3.4%, policymakers need to see more convincing progress before shifting from rhetoric to action. Consensus looks for a sizeable drop to 3%, a move that is already well priced. Therefore, a print in line with expectations would validate the current policy path but is unlikely to unlock renewed bearish pressure on the pound. Tomorrow’s labour‑market report is also highly anticipated, but continued softening remains the consensus.

With political risk receding, we expect fairly orderly price action in GBP/EUR this week, with a preference for upside should inflation fail to drop as much as forecast. For GBP/USD, the pair continues to be driven primarily by US dynamics. We see mild downside potential for the pair this week – but more as a mechanically engineered move driven by short‑squeeze flows than any shift in the underlying fundamentals, which remain broadly supportive.

EUR: Strong sentiment dominates narrative

EUR/USD remains a near‑perfect mirror of the dollar’s swings this year. Last week, the common currency pared losses endured the week prior, staying atop key daily and weekly moving averages in a sign that momentum to the upside remains.

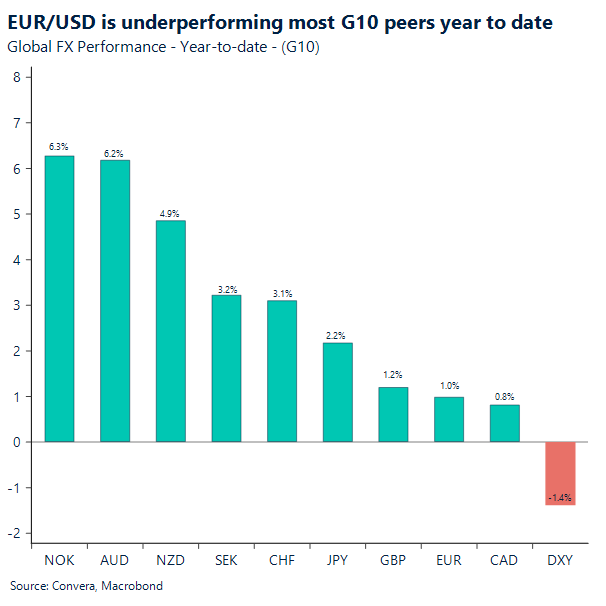

With USD sentiment soft and the US macro narrative failing to inspire, the euro remains well positioned as an attractive alternative. Even so, EUR/USD is underperforming most G10 peers year‑to‑date, up only around 1%. The pair also screens overvalued relative to macro‑warranted fair value, though this misalignment may prove more durable than initially assumed.

If the US data flow continues to disappoint and nudges the Fed toward a more dovish stance, the market’s current preference for the 1.18–1.19 area could become fundamentally justified. In that scenario, EUR/USD’s comfort at higher levels would likely persist, and a re‑test of the 1.20 handle — and potentially beyond — over the coming months cannot be ruled out.

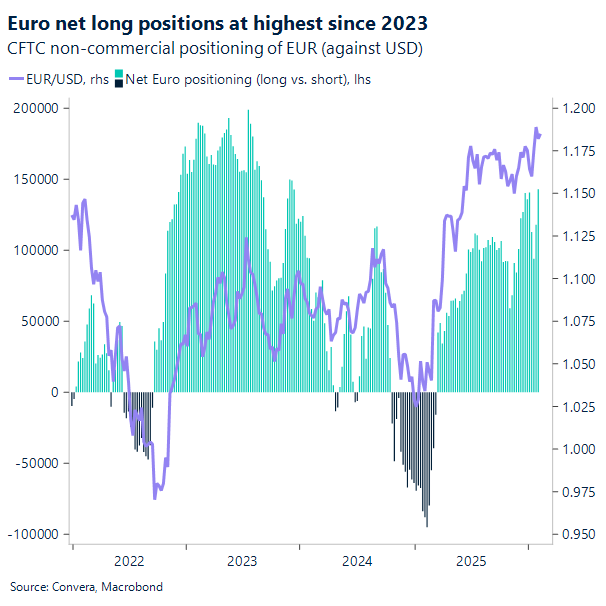

Indeed, despite only modest gains in spot and a fundamentally softer backdrop, sentiment toward the euro has turned decisively more bullish. In the FX options market, risk‑reversal pricing shows a sizeable premium for EUR upside across maturities, signalling that investors no longer view euro strength as a short‑term story. CFTC data reinforces that shift, with speculative long positions in EUR/USD at their highest since August 2023. It’s an interesting juxtaposition because the macro narrative itself doesn’t obviously justify such confidence.

ECB pricing risks still lean to the downside. Activity data has continued to lose momentum — December retail sales and the January PMIs both undershot expectations — and January’s flash CPI delivered another downside surprise, mirroring softer prints across Europe. This week’s flash PMIs for February will be key in determining whether the eurozone’s tentative stabilisation is already fading.

Yet the market’s tone remains resolutely constructive, suggesting investors are willing to look through near‑term softness and treat the euro as a relative safe harbour in a world where the US macro story is wobbling. That divergence between fundamentals and positioning is becoming a defining feature of the EUR narrative this year.

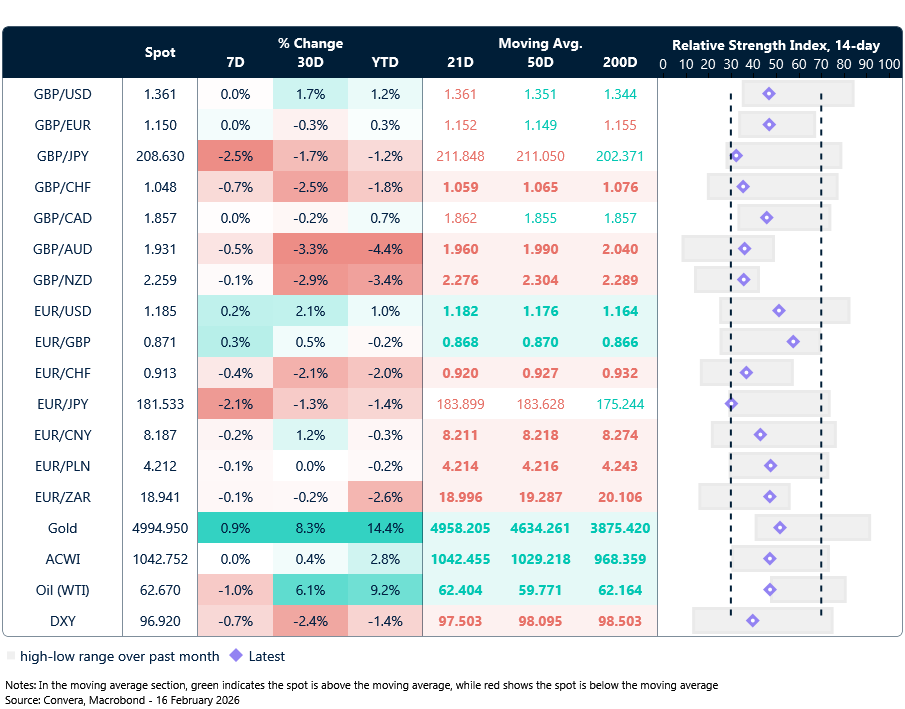

Market snapshot

Table: Currency trends, trading ranges & technical indicators

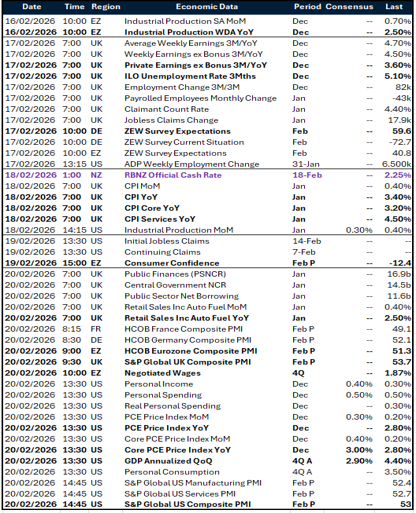

Key global risk events

Calendar: February 16-20

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.