Written by Convera’s Market Insights team

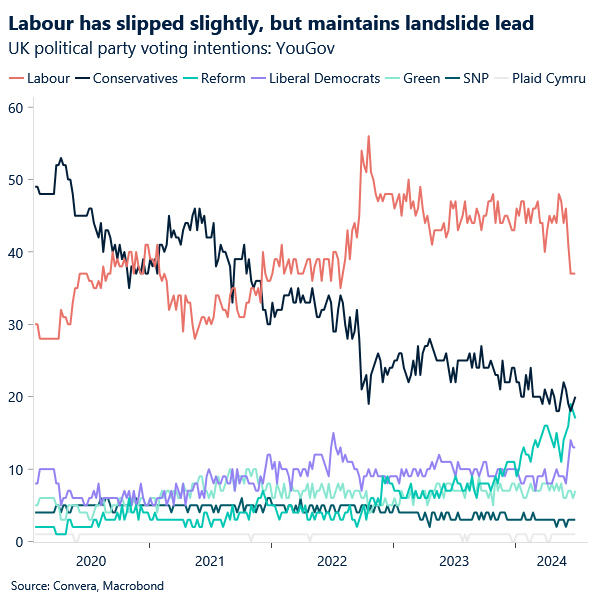

Labour tipped for historic win

George Vessey – Lead FX Strategist

Opinion polls have been remarkably consistent throughout the past six weeks. Although the opposition Labour Party has dropped four points, according to a final YouGov poll, it is still on track to become the biggest majority for any single party since 1832. The ruling Conservatives have dropped three points while the Liberal Democrats are up one and Reform UK up five. The UK’s ruling Conservatives are heading towards an electoral defeat today, but the scale of the potential rout remains unclear. Exit polls at around 10pm should give a good signal of the ultimate outcome.

How might markets react? Given the muted reaction in gilts and sterling during this election campaign, it indicates the expectation that Labour will do little to rock the fiscal boat. However, should there be a minority or coalition Labour government, markets might react negatively as this could reignite fears of political instability. Polls currently suggest a large Labour majority of 90-200 seats, with the Conservatives forecast to win anywhere between 53 and 155 seats by the different projection models. The incumbent party’s hope is that the polling industry is systematically underestimating them, as it did in 1992. But even a 1992-level polling error would leave the Tories on about 170 seats, still far short of the 325-majority needed to win. With a majority of 50-100 seats, Labour should be able to deliver on its policy agenda, with focus on continued fiscal prudence and gradual movement towards closer alignment with the European Union (EU).

This could be a positive for UK growth and it’s one reason why GBP has trended higher since the election was called, clipping 2-year peaks of €1.19 against EUR and edging closer to $1.28 versus USD. Indeed, the long-term outlook for sterling might lean more bullish given Labour’s intention to strengthen trade relations between the UK and EU. This should lead to a (partial and steady) unwinding of the pound’s Brexit premium.

Looking at FX options markets, the cost of insuring against FX volatility around the UK election date has remained relatively contained, again indicating investors are sanguine about the outcome. Where the election is more likely to impact the pound is the lifting of the Bank of England speaker blackout that we’ve had. We continue to argue that the interest rate story will ultimately determine the direction of the pound in the coming weeks and months so markets will welcome some fresh guidance ahead of the BoE’s next meeting in August.

Dollar slumps after data misses

George Vessey – Lead FX Strategist

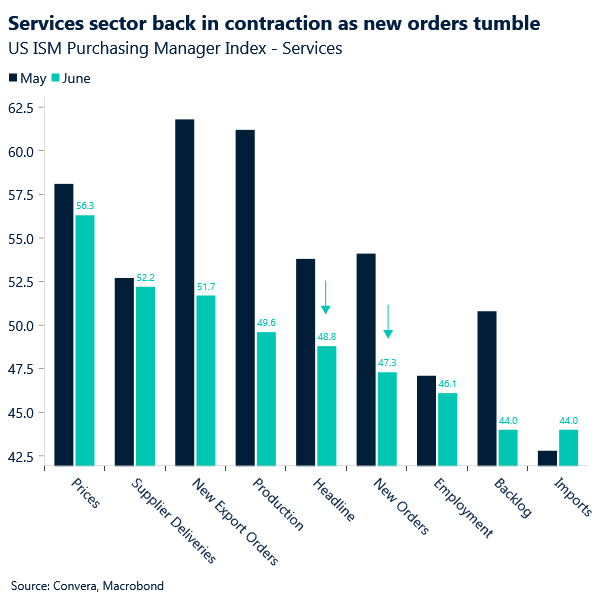

The US dollar suffered its biggest daily drop in three weeks yesterday and Treasury yields edged closer to 3-month lows whilst equities remained close to their all-time highs. Why? A string of weaker-than-estimated US economic data, particularly from the services sector – the engine of US economic growth, reinforced the case for the Federal Reserve (Fed) to start cutting rates in September.

With French political risk premiums easing a bit, reducing safe haven demand and supporting the euro, it has been the rising probability of a Trump presidency keeping the dollar afloat. But now US macro weakness is dominating again. Data on Wednesday offered more evidence of a cooling economy and softening jobs market. The ADP report showed fewer job gains than expected, while continuing jobless claims increased for a ninth straight week and to the highest level since 2021. But the big move in markets came after the ISM services PMI print of 48.8 versus 53.8 prior, highlighted the services sector contracted at the fastest pace in four years. New orders, dropped sharply to 47.3, the lowest reading since December 2022. The downshift in US labour indicators, coupled with slowing economic activity and disinflation being back on track resulted in yields across the maturity spectrum falling as the probability of a September Fed rate cut jumped from around 60% to over 70%.

It’s US Independence Day today, so with US markets closed liquidity could be thin, but investors and policymakers will get further insight into the state of the US labour market on Friday with the release of the monthly employment report. If the data cooperate, increasing speculation about two cuts this year, dollar weakness could extend into next week, but it’s still too soon to call sustained USD depreciation.

EUR/USD propels as US data disappoints

Ruta Prieskienyte – Lead FX Strategist

The euro rallied to a three-week high amid a significant dollar weakness stemming from growing expectations of a Fed rate cut in September following a streak of disappointing economic data. The risk on environment characterised by rising equities and falling bond yields proved a favourable backdrop for risk assets. DE-US 2-year yield spread tightened to 180bps, a near 3-week low, in support for the euro.

Data wise, the HCOB Composite PMI for Eurozone was revised slightly higher to 50.9 in June, up from a preliminary print of 50.8. The reading pointed to continued growth in the private sector, although the expansion cooled to a three-month low. On the political front, the French media reported that between 214 and 218 third-placed contenders had pulled out of the race in their constituencies. This means Marine Le Pen’s party needs 289 seats to win an absolute majority in the National Assembly. The spread between OAT-Bund 10-year yields, a proxy for the French risk election premium, further narrowed to 66bps from a high of 82bps towards the end of last month. We should, however, expect to see the euro volatility returning closer to second round runoff this Sunday (7 Jul).

As the US markets are shut and the domestic calendar is largely absent of top tier data releases, we expect yesterday’s euro strength to wane somewhat, as it has already met waning interest at the $1.08 barrier and realised FX volatility to retreat. The risk reversals for EUR/USD remain stable on a 1-week tenure with the second round of the French parliamentary elections just a few days away but we have seen a growing euro optimism in the options market. Namely, the 1-month EUR/USD risk reversal shifted to the least euro bearish sentiment in over three weeks, tightening to -0.498 in favour of euro puts. Elsewhere, The UK general elections will determine the direction of the EUR/GBP pair going into the weekend. The overnight EUR/GBP volatility traded at 3.19% vol, indicating that markets participants are not expecting a surprise outcome. With the Labour party almost certain to take the reins of the new UK government, such an outcome would be Sterling positive and we could see EUR/GBP decline further in the short term.

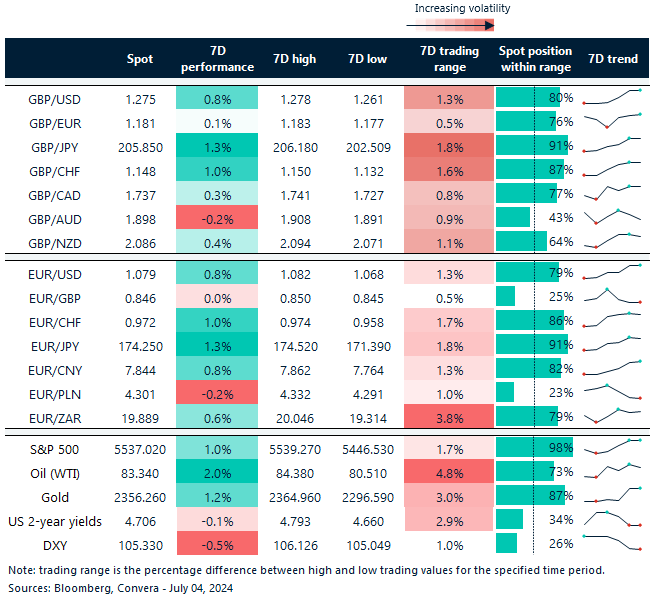

Pound in higher realms of recent trading ranges

Table: 7-day currency trends and trading ranges

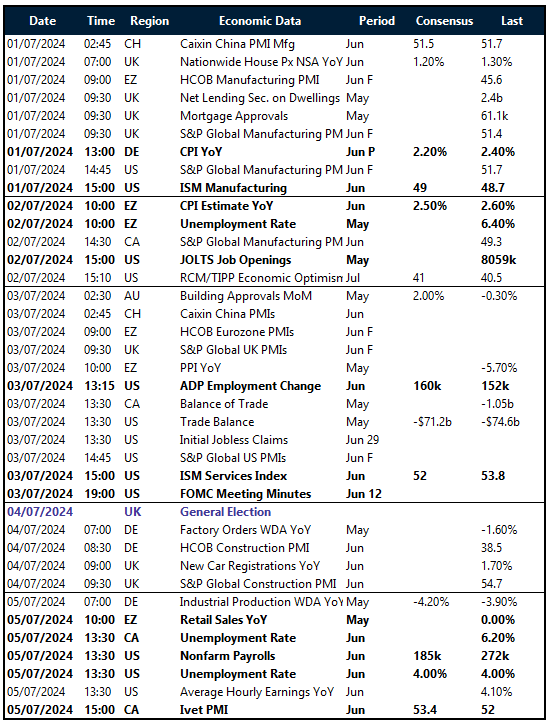

Key global risk events

Calendar: July 01-05

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.