Middle East conflict: Sudden war reshapes global outlook

The sudden shift from hopes of significant progress in negotiations between the US and Iran, to a full-scale leadership campaign has caught global markets completely off guard. While investors were leaning into a diplomatic resolution just days ago, the reality of current operations has shattered the belief that these regional tensions can be easily boxed in. Unlike the narrow raids of the recent past which were largely seen as insignificant from a macro standpoint, the current focus on neutralizing core political targets is inherently harder for the market to price than any tactical strike we have seen. This is no longer just another page from the standard geopolitical playbook but a fundamental move that puts every previous assumption of containment at risk.

This escalation places the energy market at the absolute center of the macro conversation, specifically regarding the Strait of Hormuz. This waterway handles roughly twenty million barrels of oil every day, serving as the world’s most critical chokepoint by carrying about one fifth of total global consumption. While pipeline alternatives through neighboring countries can offer a bit of a buffer, they simply cannot fully replace the massive volumes moving through the water if the situation continues to intensify. What was once considered a remote tail risk has moved uncomfortably close to a base case, with rising insurance costs and shipping delays likely to keep an energy risk premium alive much longer than in past cycles.

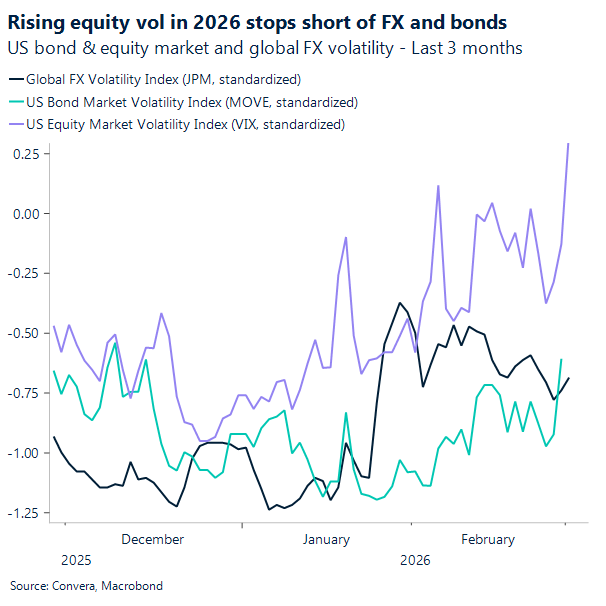

Many investors are reflexively looking to sell the risk premium because history shows the S&P 500 barely flinched during previous episodes like the Abqaiq strikes. Also, there is a strong argument that AI capital expenditure intentions and underlying stress in private credit markets are actually more vital to the long-term economic outlook than oil volatility, leading many to believe history will simply repeat itself. However, the real danger is that this learned behavior leaves the market totally unprepared for a scenario where containment actually fails. If casualties mount or the conflict escalates or takes several weeks, the eventual repricing will be far more painful precisely because so many participants are positioned for a quick bounce that may not arrive.

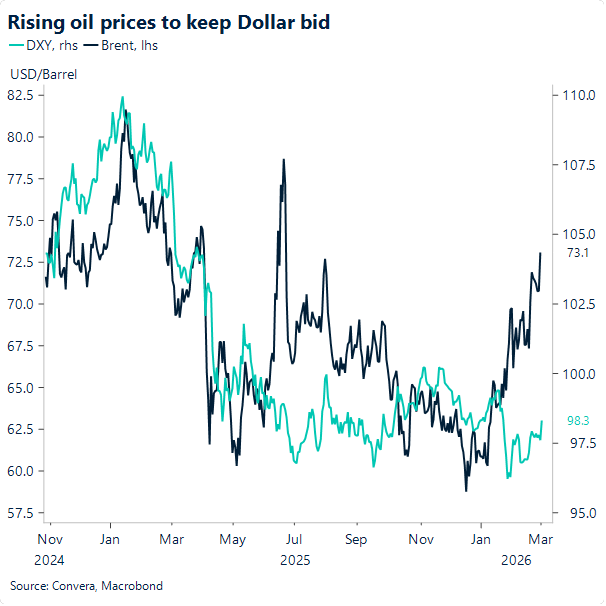

In this environment, this week, standard economic data reports, such as the NFP payrolls report, will likely be ignored in favor of the regional conflict headlines. We expect a direct correlation where the dollar typically benefits, fueled by both higher costs and a rush for safety. While energy sensitive currencies like the Yen may weaken enough to bring the currency closer to intervention territory, the dominant force remains the global scramble for liquidity. Ultimately, the length and breadth of the hostilities will dictate how long these premiums last, but for now, the flight to quality is the trade that matters.

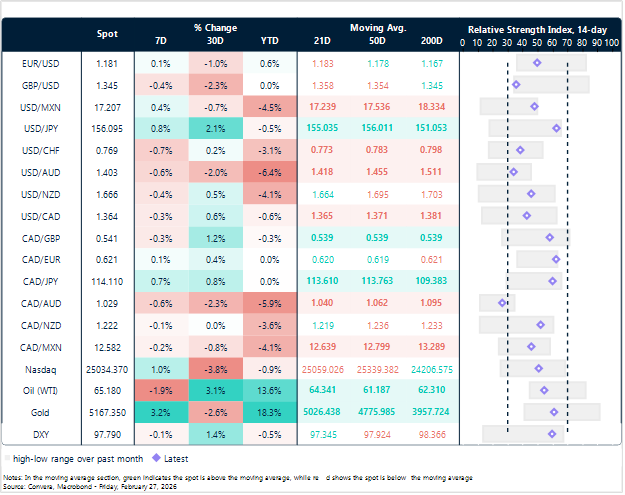

What’s the FX outlook as these Middle East tensions escalate? The Euro, trading 0.8% down today, as major LNG and oil importer should stay offered, similar to the Japanese Yen, losing 0.7% today as a major oil importer. The Swiss Franc, which was expected to gain on safe-haven flows, is losing today instead 1%, after the Swiss National Bank said it was prepared to intervene in FX markets. Among commodity currencies, the Canadian Dollar is outperforming the Aussie and Kiwi but remains weaker against the US Dollar.

AI: AI narrative fragility, and the HALO shift

The release of Citrini Research’s The 2028 Global Intelligence Crisis has become a lightning rod for a set of anxieties that were already embedded in the 2026 market tape. Its “nightmare scenario”, AI-driven displacement pushing unemployment to 10%, compressing consumer demand, and dragging the S&P 500 into a drawdown, doesn’t merely describe a macro-outcome. It implicitly elevates a single interpretation of AI: not as a general-purpose technology that expands the frontier, but as a disruption engine that destroys value faster than it creates it. The market’s reaction has been less about proving the report right than about revealing how primed investors are to believe the downside narrative, especially where business models look easiest to digitize, replicate, or disintermediate.

That asymmetry has been visible for a while. In 2025, the Philadelphia Semiconductor Index surged while broad software lagged, a dispersion that reads like a market verdict on what is certain versus what is speculative. Compute, chips, power, data centers, must be built in the physical world, on constrained timelines, with real balance-sheet costs. Much of application software, by contrast, sits atop business models that can be repriced overnight if users believe agents will collapse switching costs or commoditize workflows. Citrini’s report didn’t create that fear; it gave it a narrative, and narratives are a powerful short-term input into market pricing.

The episode also highlights an uncomfortable feature of today’s market structure: narrative fragility. When a “think piece”, (or a sci-fi piece?), can trigger sharp single-day repricing across software and services, the message isn’t that the analysis is definitively correct; it’s that investors are treating AI as a regime change where the distribution of outcomes has fat tails. In that environment, companies perceived as “prompt-replaceable” trade less like cash-flow streams and more like exposures to technological obsolescence. Even if the underlying businesses are resilient, their multiples become vulnerable to any story that plausibly claims an agent can do the job.

But there is an equally important counterpoint: the market is reacting to a future that is not yet visible in the macro data. Adoption is broad, yet aggregate impact remains elusive. Executive surveys suggest a large share of firms are already using AI, while measured productivity effects over the last several years have been modest. Even where official productivity readings have improved, U.S. total factor productivity rising in 2024, for example, the leap from “promising micro gains” to “economy-wide step-change” is still more expectation than observation. That gap matters because it creates the perfect conditions for anxiety: a historic shift that everyone can feel, but few can quantify.

This is where the infrastructure buildout becomes both the bull case and the bear case. On one hand, hyperscalers are committing to extraordinary capital expenditure plans, effectively industrializing the inputs to intelligence, compute density, data center footprints, and model deployment capacity. If AI becomes embedded across workflows, the return opportunity is enormous. On the other hand, when markets cannot yet see the productivity dividend, the same capex numbers can look like the early stages of a capital overhang: supply ramping faster than monetization clarity. The result is a bifurcated psychology, confidence in the picks-and-shovels layer, skepticism about who captures value at the application layer, and deep uncertainty about the pace of demand realization.

Inside firms, however, the evidence is less apocalyptic and more nuanced. Randomized field experiments and real-world deployments increasingly suggest that generative tools can deliver material task-level productivity gains, especially when paired with oversight and when applied to well-scoped work (coding assistance, customer support, knowledge retrieval, internal copilots). The pattern is consistent: the tool raises throughput, the biggest gains often accrue to less-experienced workers, and the binding constraint becomes governance, workflow integration, and quality control, not the raw capability of the model. In other words, AI looks less like a pure labor replacement machine and more like a leverage amplifier, but one that requires organizational redesign to convert time saved into output gained.

That distinction is central to the disagreement between “value destruction” and “value creation.” Citrini’s scenario implicitly assumes a world where AI substitutes broadly for labor faster than economies can adapt. The counterpoint by contrast, rests on a historical regularity: technology eliminates tasks and roles, but it also creates new categories of work and expands activity where costs fall. The tension can be framed cleanly through two competing intuitions:

• The “post-labor” fear: AI removes so much work so quickly that labor demand collapses before new sectors absorb displaced workers.

• The Jevons/expansion view: as AI makes tasks cheaper and easier, the volume of activity increases, sometimes dramatically, creating new coordination, oversight, compliance, customization, and human-in-the-loop roles.

A concrete example is legal work. If AI compresses the cost of drafting, discovery review, or basic motion practice, one possibility is fewer billable hours. Another is more litigation, more disputes pursued, more compliance activity, more contract iteration, because the cost barrier falls. The economic question isn’t whether AI saves time; it’s whether institutions convert time savings into fewer workers, or into more output, more services, and new categories of demand. That is an adoption and incentives problem, not merely a model-capabilities problem.

As Josh Brown, CEO of Ritholtz Wealth Management has brilliantly put it, the market’s pivot toward HALO, Heavy Assets, Low Obsolescence, fits neatly into this uncertainty. HALO is not just a style shift; it is an implicit hedge against “promptability.” If investors believe certain digital workflows will be absorbed into general-purpose agents, they will demand a higher risk premium from businesses whose differentiation is primarily informational or intermediary. Conversely, they will pay up for assets that are hard to replicate digitally: physical networks, regulated infrastructure, manufacturing capacity, energy systems, transportation fleets, and branded consumer products with distribution moats. “You can’t prompt a soda can” becomes not a quip, but an allocation rule.

Yet HALO can also become an overcorrection if it collapses everything into a single dimension of risk. The reality is more layered. Some “asset-light” firms will defend moats through proprietary data, integration depth, distribution, compliance, and embedded workflow ownership. Some “heavy asset” firms will still face margin pressure if AI improves procurement, reduces coordination costs, and intensifies competition. HALO is a useful prism, but not a substitute for asking the deeper questions: Where does pricing power sit in the AI stack? Who owns the customer relationship, the workflow? Who bears the capex and captures the surplus?

This is why the present moment feels like a regime change in market logic. Traditional categories, growth versus value, cyclical versus defensive, don’t fully describe what is being repriced. The new axis is obsolescence risk versus physical or institutional moats, and the market is trying to map it in real time with incomplete information. Supportive macro conditions, cooling inflation, a central bank with room to cut, and still-firm activity, can cushion the cycle, but they cannot resolve the structural question of how fast AI changes unit economics across industries.

In the end, the most coherent interpretation of the current landscape is not “AI will obviously destroy everything” or “AI will obviously create everything.” It is that AI is a general-purpose technology whose value creation will be real but uneven, whose value destruction will be localized but violent, and whose market pricing will remain fragile until measurable productivity and earnings diffusion catch up with narrative velocity. That is why the tape feels confused: the market is discounting a shifting map of which cash flows are defendable. And as Brown puts it, it isn’t supposed to be easy, because the investment problem is no longer forecasting growth. It is forecasting who keeps the growth.

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

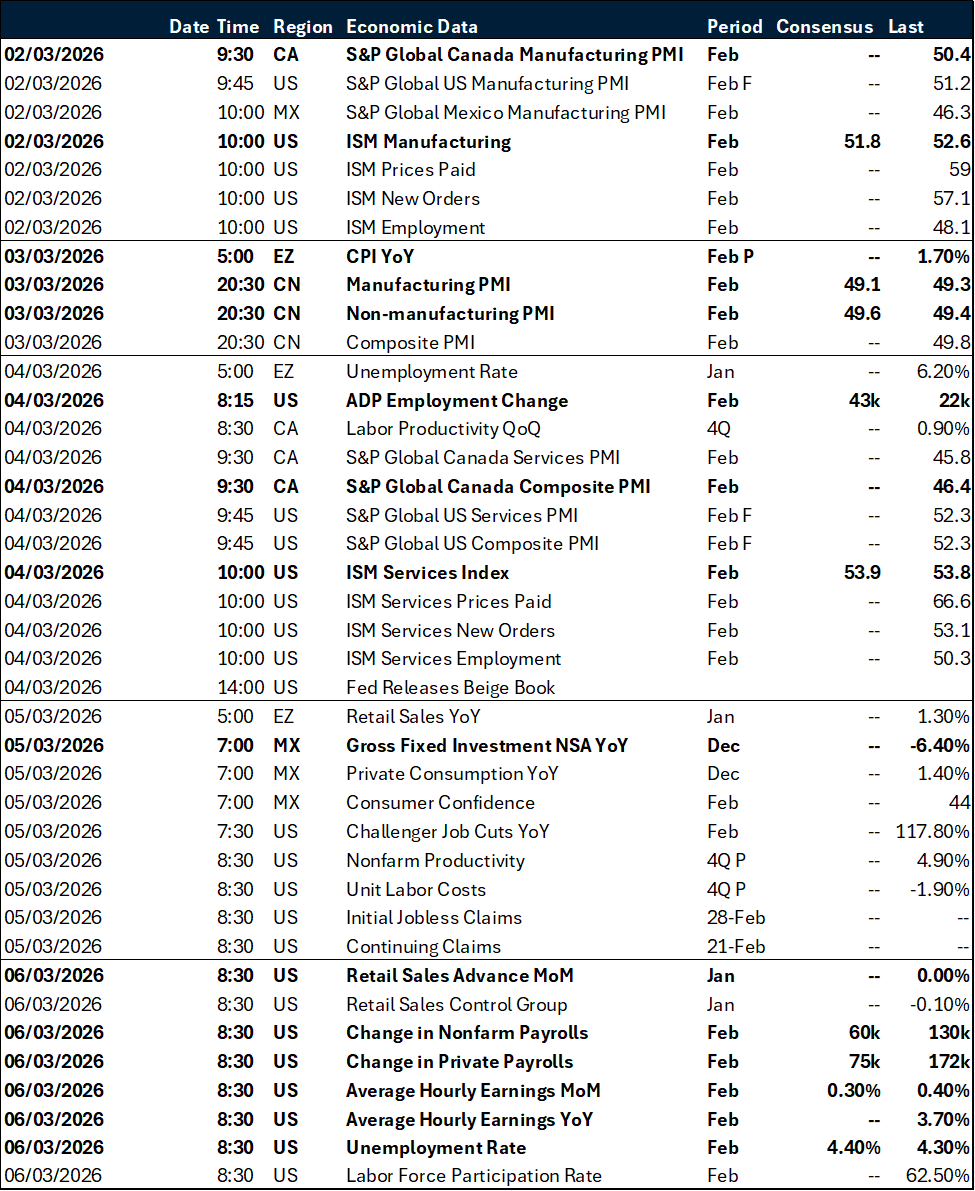

Calendar: March 2 – 6

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.