Tariff deadline looms

The Australian and New Zealand dollars fell for a second day on Friday as financial markets turned more nervous ahead of Wednesday’s tariff deadline.

US president Donald Trump announced a 90-day suspension of his tariff program that is due to expire on 9 July and last week President Trump said a series of letters outlining the new tariff rules will be sent to trading partners on Monday.

The AUDUSD fell 0.2% as the pair slipped from the eight-month highs seen last week.

The NZD/USD also fell 0.2% as the kiwi dropped from nine-month highs.

USD/SGD rebounds from decade lows

In Asia, the greenback was mostly weaker on Friday, driven by losses in USD/JPY

The USD/SGD and USD/CNH both fell around 0.1% on Friday, but notably rebounded from lows last week.

Atlanta Fed President Bostic, though not a voting member, sees pricing pressure sticking around due to ongoing uncertainty over future tariffs and their effect on consumers.

The USD/SGD has now snapped back from its decade-low of 1.2698.

With momentum shifting, dollar buyers might look to take advantage of current levels.

Next key resistance lies at the 21-day EMA of 1.2801, and 50-day EMA of 1.2906 next.

RBA, RBNZ due this week

The upcoming week will see inflation data take centre stage, with key releases from China, Japan, and Europe.

China’s CPI YoY and PPI YoY for June are due on Wednesday, with CPI expected to remain flat at 0% and PPI to show continued deflationary pressures at -3.1% (previous: -3.3%). Japan will release its PPI YoY on Thursday, with consensus at 2.9% (previous: 3.2%).

Meanwhile, Germany, and France will publish their final June inflation figures on Friday, providing further insights into price pressures across Europe.

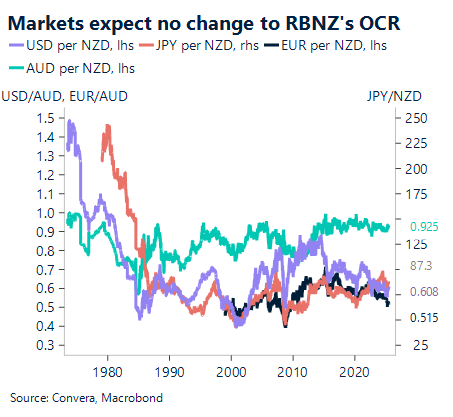

The Reserve Bank of Australia (RBA) and the Reserve Bank of New Zealand (RBNZ) are set to announce their monetary policy decisions this week. The RBA is expected to cut its cash rate target to 3.6% on Tuesday.

The RBNZ will announce its decision on Wednesday, with markets anticipating no change to the official cash rate, which currently stands at 3.25%. These decisions will be closely watched for any forward guidance on future policy moves.

Growth indicators will also be in focus, with Germany’s industrial production data for May due on Monday, following a contraction of -1.4% in the prior month. The UK will release its monthly GDP for May on Friday, alongside industrial production and manufacturing production figures.

Greenback stages comeback ahead of tariff news

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 7 – 12 July

All times AEST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.