Written by the Market Insights Team

Markets’ hope for salvation

Kevin Ford – FX & Macro Strategist

The trajectory of global markets hinges on three critical drivers—each offering little hope of materializing in the near term:

1. The “Trump Put”: A shift in rhetoric or mentions of negotiations with major trading partners could provide some relief, as markets hope that tariffs serve as both structural reforms and tactical bargaining tools. However, President Trump has made it clear that tariffs are here to stay. Commerce Secretary Howard Lutnick has outlined the administration’s expectations for reciprocal tariffs, emphasizing a focus on addressing non-tariff trade barriers as part of a broader “reordering of fair trade.” Lutnick anticipates that most countries will reassess their trade policies toward the U.S., with negotiations only likely if significant changes are made to tariffs and trade barriers.

Also, while equity markets have reacted sharply, President Trump ’47 differs notably from his earlier term. He has consistently downplayed market reactions, prioritizing lower interest rates, declining oil prices, and reduced costs for essentials like eggs. He has reiterated that he won’t yield to market pressures, framing short-term disruptions as acceptable trade-offs for long-term goals.

2. The “Fed Put”: Investors are eyeing the possibility of an emergency rate cut or liquidity injection to stabilize markets. President Trump has publicly urged Fed Chair Jerome Powell to lower rates via social media. However, the Fed faces a challenging balancing act. Despite lagging indicators, job data still suggests stability, complicating the risk assessment between employment and inflation. There are rumors of a potential meeting of the Federal Reserve Board of Governors ahead of their scheduled May 7 meeting. Still, a rate cut in May seems unlikely, even after the S&P’s recent 10%+ drop.

3. Hard Data: While high inflation and low growth are widely expected, the looming question remains whether a recession is on the horizon. Historically, the U.S. labor market has been a lagging indicator. For instance, the jobless rate was just 6.1% in September 2008 but peaked at 10% in late 2009. Consumption, particularly for big-ticket items like automobiles, is likely to respond more swiftly to economic shifts. The reality is that, we’re still away from a recession in 2025, even as odds have risen recently.

The situation remains highly fluid, with tensions escalating on multiple fronts. Vietnam—one of the nations hit hardest by tariffs—offers a compelling case study for market adaptation. President Trump recently hinted at progress in trade discussions with Vietnam’s leader via social media, though he emphasized that this does not signal an immediate lifting of tariffs on the country.

Meanwhile, domestic political pressure is intensifying. Senator Cruz, usually a firm ally of President Trump, has raised alarm over a possible “midterm bloodbath.” This comes amid growing dissent among Republicans, with four senators already breaking ranks to oppose tariffs on Canada.

In FX, the last couple of sessions have seen some swings, with the dollar steadily regaining its reputation as a reliable safe haven. However, as global market fears ease briefly, the dollar’s moves remain erratic, giving back part of its recent gains.

Markets whipsaw on conflicting headlines

George Vessey – Lead FX & Macro Strategist

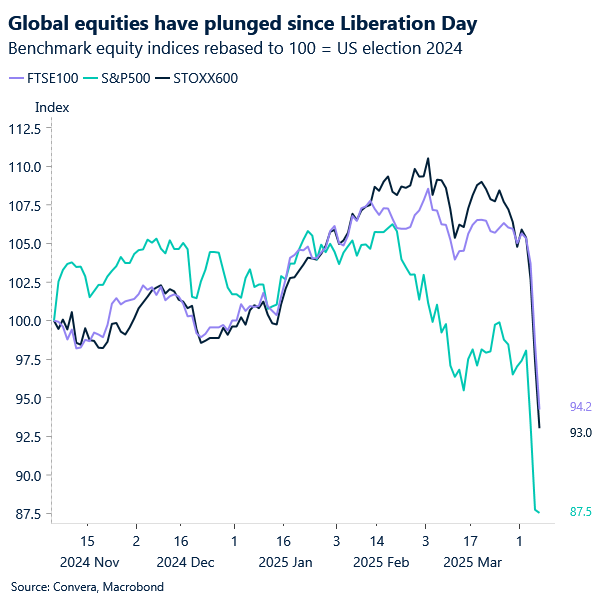

Financial markets experienced more turbulence on what was a manic Monday, with equities swinging between sharp gains and losses on tariff related headlines. But safe haven bonds are being dumped too, with the 10-year Treasury yield jumping sharply back above 4% in what was the biggest single daily gain in almost three years. The US dollar remains under pressure despite its haven status, whilst the Swiss franc is emerging as the safest bet in the FX space.

Rumours of a 90-day tariff pause sparked a global risk rally before the White House declared “fake news”. Equity declines then extended after President Trump threatened to impose additional tariffs of 50% on China unless Beijing withdraws its 34% retaliatory duty on US goods. These measures, combined with existing tariffs, highlight the administration’s determination to impose duties on virtually all trading partners.

The Nasdaq Composite was swinging from a 4.5% gain to a loss of around 5% at Monday’s intraday extremes, putting it on pace for the most dramatic intraday spread since November 2008. In the FX markets, safe haven demand soared, mostly benefiting the Swiss franc, surging 3.5% since last week against the USD and not far from levels that have proved to be unsustainable in the past.

Price action is already reminiscent of significant dislocations like Covid and the global financial crisis. Volatility is rife, and it may remain this way until we get more clarity on the ultimate level and duration of tariffs. The elevated volatility, reflected in the VIX reaching crisis-level readings, underscores the precarious state of financial markets.

Europe to vote on retaliation measures

George Vessey – Lead FX & Macro Strategist

In Europe, the Stoxx 50 plunged more than 7% before closing 5.4% lower, its lowest since August. The Stoxx 600 fell as much as 6% before narrowing losses to end 4.5% down, its lowest since January 2024. The euro didn’t escape the FX volatility, but it proved resilient – holding above the $1.09 handle versus the US dollar whilst rising to a 6-month high against the pound.

It’s been an abrupt reversal for European stocks. After riding on optimism in past weeks over talks of German fiscal reforms and European investment in defence, Trump’s tariffs have now triggered a market rout. The situation remains extremely fluid though. At one point, headlines revealed the EU was looking at reducing its retaliation against US steel tariffs after member states lobbied to protect their industries. But now, it appears the bloc is planning 25% tariffs on a range of US products – from yachts to tobacco. The total amount of US exports affected would be €22.1 billion based on the EU’s 2024 imports, according to public Eurostat figures. EU governments will vote on the plan on Wednesday.

In terms of where that leaves the euro – it’s still a tug of war between tariff pain and the fiscal response from Europe. Although a global trade war would typically weigh on the euro, the vulnerabilities in the US economy and the fiscal response from Europe are currently the driving force for EUR/USD, keeping it supported more than other major currencies outside the typical safe havens.

Tariff haven no more

George Vessey – Lead FX & Macro Strategist

Sterling’s resilience to tariff risks has come to an end. GBP/USD sunk over 1% on Monday to touch its lowest level in five weeks – extending its drop from $1.32 touched just last Thursday. GBP/EUR also dropped around 1%, failing to hold above its 200-week moving average at €1.17, and breaking below a long-term upward sloping trendline that’s been in place since late 2022.

Although the UK has been slapped with the lowest tariff rate of 10%, it will still suffer from a global trade war and global economic slowdown. Ultimately the pound is a pro-cyclical currency that usually appreciates in good times and depreciates in bad times. With global investor sentiment so weak and volatility so elevated, it was only a matter of time before investor ditched the UK currency in favour of safer alternatives with current account surpluses.

The threat of the economic slowdown spilling into the UK is why markets also anticipate more Bank of England (BoE) rate cuts. Markets are now pricing in around 88 basis points of reductions to the BoE’s benchmark rate by December, up from about 43 basis points at the end of March. The likelihood of a 25-basis-point rate cut at the BoE’s next policy meeting in May has also surged to around 90%.

In a context where safe-haven demand continues to dictate sentiment amid the chaos of US tariffs FX traders are turning more bearish on the pound, especially since both GBP/USD and GBP/EUR have broken below their 200-day moving averages. Sterling will require a rebound in global risk appetite in order to claw back recent losses.

Euro resilient against most peers

Table: 7-day currency trends and trading ranges

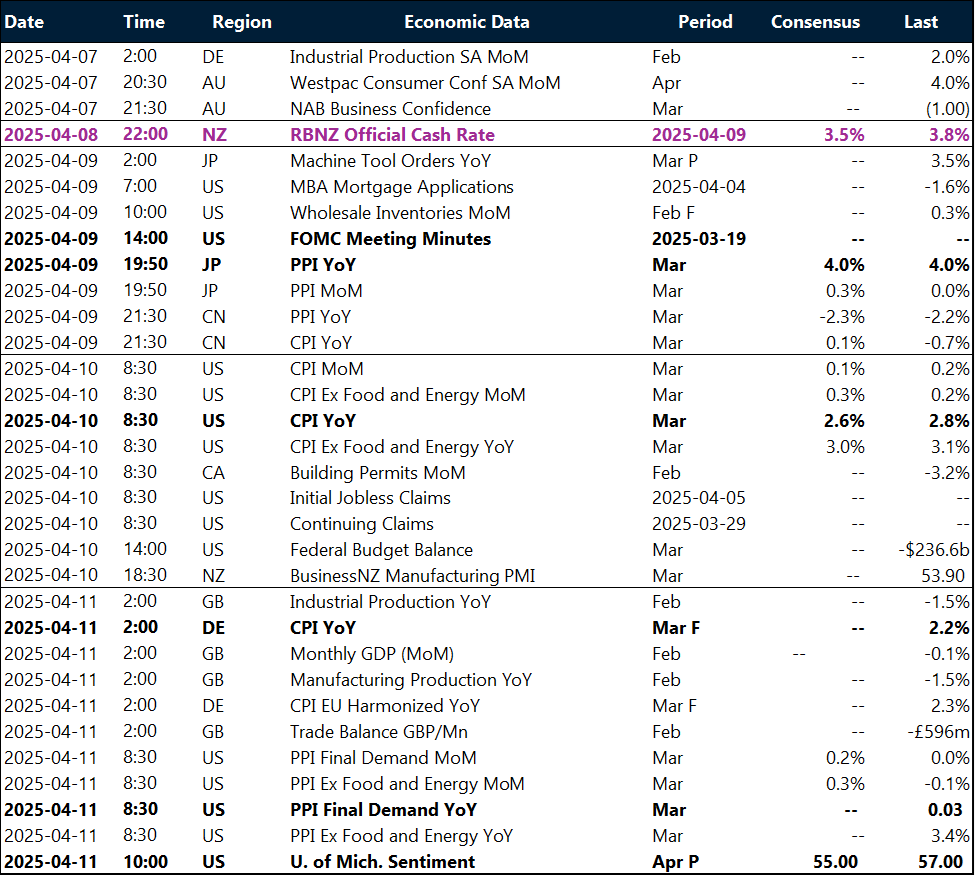

Key global risk events

Calendar: April 7-11

All times are in ET

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.