Euro unresponsive to higher yields

Germany has fallen into recession, but the hawks within the ECB’s governing council don’t seem to be backing down from their calls to continue raising interest rates. While price pressures have been trending down in the US, inflation in the Eurozone is still hovering near record levels. Bundesbank president Joachim Nagel continues to shape the hawkish narrative and still sees three rate hikes as possible, while the Dutch governor focused more on being restrictive for a long period after reaching the peak level.

Markets are currently pricing in 50 basis points of hikes from the ECB, mainly in line with economists consensus. While todays calendar is lacking any significant macro data in Europe, next week will see the release of inflation. The print will be important as the ECB is still uncertain about the extent of its commitment to raise interest rates further.

So, why has the Euro become unresponsive to hawkish talk and higher yields? Simply because of (1) the deterioration of the global economic outlook with Germany and China at the center of this narrative and (2) the repricing of Fed policy higher outweighing any increase in European rates. Yields on 2-year government bonds have risen by around 27 basis points more in the US – up ten days in a row – compared to Germany during the last three weeks. EUR/USD has fallen 2.7% in the same period.

Yield explosion unable to help the pound

Two-year UK government bond yields are on track to rise by 57 basis points, the highest weekly increase since the crisis in September. A weekly close at levels above 4.4% would also be the highest level yields have traded since 2004. The pound has not been able to benefit from higher rates, given that a continued tightening of monetary policy might drag economic growth down in the process.

While inflation rates are trending down globally, most central banks still have a long way to their inflation targets. Only 16% of countries worldwide have an inflation rate of below 4%, while 44% continue to struggle with inflation above 8%. The latest CPI surprise in the United Kingdom shows how sticky inflation can change narratives and impact market positioning through various asset classes (equities, fixed income and FX).

Today’s release of retail sales adds fuel to the idea, that the consumer is still holding up. Volumes of goods sold in stores and online increased by 0.5%, more than expected. Markets have now increased their expectations of the peak interest rate from 4.5% in September to 5.5%. GBP/USD bounced back slightly off the support level at $1.23 coming from the upward trend line that started in September.

Treasury cash reserves plunge below $50 billion

Policy makers in Washington have been moving closer on reaching an agreement to raising the debt ceiling, that would raise the debt limit for two years. However, the deadline laid out by treasury secretary Janet Yellen is less than one week away and with the treasury’s cash reserves plunging to below $50 billion, market stress remains elevated. This can be seen when looking at 1-month treasury bills, which briefly surpassed the 6 percent mark this week.

On the economic front, macro data has been holding up against the headwind of political uncertainties and higher interest rates. The labor market in the US continues to show signs of resilience and has been making the Fed’s job of fighting inflation a difficult one. The number of citizens claiming unemployment benefits rose to 229 thousand last week. While marginally higher than previously, these levels are nowhere near recessionary territory. Gross domestic product for Q1 rose by an annualized rate of 1.3% and therefore a bit better than initially expected. Corporate profits, however, fell by 6.8% during the first three months of the year, well below the consensus forecast of a 0.9% contraction.

The US dollar is expected to record the third week of gains against a basket of major currencies after having risen from Monday to Thursday. However, today’s weaker open indicates some pushback for levels above 104.30 at the aggregate level (US Dollar Index, DXY). In terms of EUR/USD, $1.0740 is now the level to beat, if the dollar uptrend is to continue next week. The release of the highly anticipated US PCE inflation will close out the week. Given the recent repricing of yields and rates expectations higher, a disappointing inflation print might make or break the rally of the dollar we have seen this week.

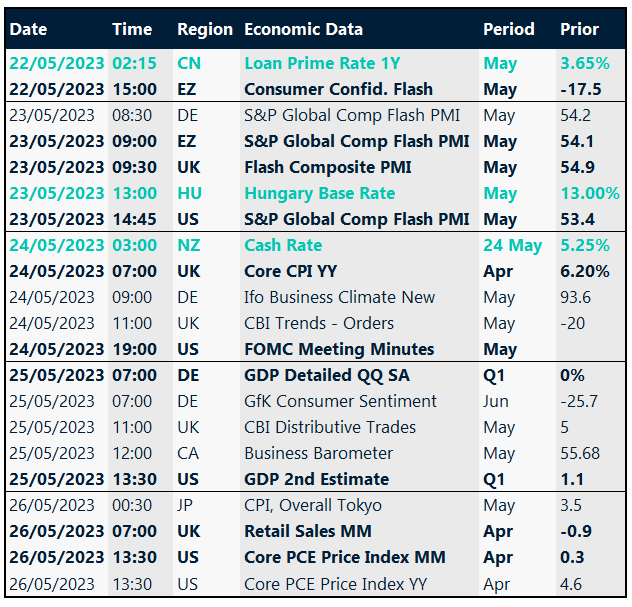

Key global risk events

Calendar: May 22-26

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.