This article is part of a series of topical blogs exploring key insights from our Fintech2025+ report, which is available to download now.

The digital economy is transforming the landscape of student mobility and international payments. Since 1998, the number of international students has more than tripled, and despite recent economic challenges, projections indicate robust growth in student mobility and associated cross-border payments. This presents opportunities and challenges for education institutions, who are facing the expectations of students familiar with fintech innovations such as real-time payments, digital wallets, and central bank digital currencies.

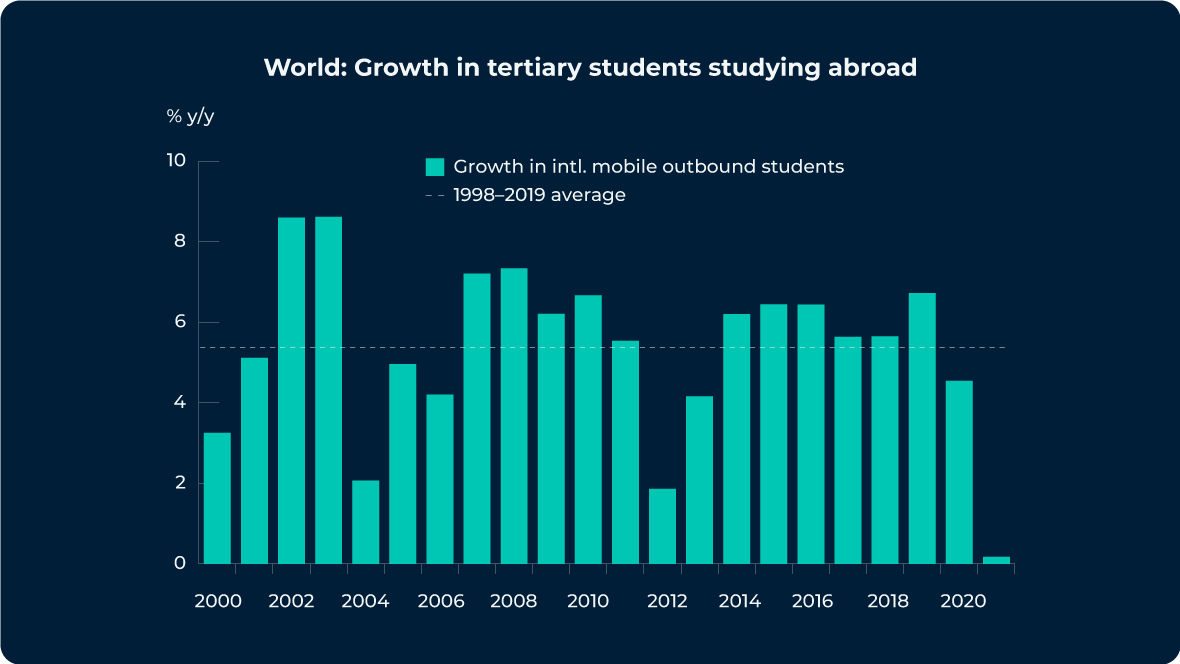

Long-term growth in international students

In 1998, when UNESCO records began, there were just under two million international students enrolled globally. By 2020, this number had more than tripled to 6.4 million driven by an increasingly globalized world economy and access to financial aid for international students.

Growth in outbound students has now exceeded global (real) GDP growth. However, when viewed through an alternative GDP measure weighted by outbound students, there is a strikingly close correlation between the two. This indicates that when analyzed through a more nuanced lens, macroeconomic conditions in sending countries have been very strongly correlated with international student volumes at the global level since UNESCO records began.

That said, the economic shocks of the past few years have had an impact. The world’s largest outbound student markets faced a considerable slowdown in real household disposable income growth in the 2021–23 period compared to the average rate of growth over the last two decades. This implies a recent slowdown in outbound students most pronounced in China, South Korea, the US and Nigeria, and less severe in other major outbound markets such as India and Vietnam.

Continued robust growth expected in international students

Despite this dampening of growth in certain outbound countries, the Fintech 2025+ report suggests that in the period to 2030 global outbound student volumes will grow at an average rate of 4 – 4.5% per year.

China and India are expected to remain the leading senders of international students. Although other countries may experience stronger economic and demographic growth, the sheer scale of China and India means their slower growth rates will still result in significantly higher student mobility volumes.

Meanwhile, student mobility in Brazil and Pakistan is expected to exceed historical growth rates despite facing various macroeconomic challenges. Although overshadowed by the likes of India and China, Brazil is a sturdy source of international students contributing approximately 90,000 individuals to the market.

In 2023, over 1 million Chinese students were studying abroad, while the number of international students from India totaled over 516,000, a figure expected to increase based on the country’s rapidly growing middle class.

Student mobility and cross border payments growth

According to Oxford Economics’ research for the Fintech 2025+ report, total cross border payment flows are expected to reach $290 trillion by 2030. Given robust (albeit moderating) growth in the international student market, it’s expected that education-related cross-border payments should also continue to grow at a solid pace.

Initiatives are being developed by the G20 to enhance cross-border payments, by addressing issues like high costs and low speed.

Growth in cross-border payments will vary by region, with prospects brightest for payment corridors in Asia-Pacific, which is forecast to be the fastest-growing region. This reflects the region’s rapid economic growth, and advances in infrastructure and payments technologies facilitated by collaboration between regional governments.

Five of the top ten outbound student markets are situated in Asia Pacific, suggesting that student mobility has a role to play in the growth of cross border payments in the region. Asia Pacific is also leading the way in payments innovation, showing significant adoption of real time payments, digital wallets, and advancements in blockchain technology such as central bank digital currencies (CBDC).

The region’s progressive stance on the digital economy means that education institutions must be prepared to meet the advanced payment needs of international students from top outbound markets such as China and India.

Central bank digital currencies (CBDCs), and China’s alternative payments ecosystem

Cash is on the outer in China, with US$434 trillion transacted electronically every year according to UnionPay, and over 80% of daily consumption transactions done via mobile platforms.

China relies on an alternative payment system built on digital wallets running through Alipay and WeChat Pay. Together these two companies own over 90% of the country’s digital payment market, creating an ecosystem that bypasses intermediary banks and financial institutions, and creates different incentives between merchants, consumers, and payment system providers.

Fuelled by integration with digital wallets, China is also among the top five real time payment (RTP) markets, estimated at USD 5.46 billion. To enhance RTPs and advocate for the internationalization of the yuan, China has built a cross border interbank payment system (CIPS). This also functions as an alternative payment system that allows countries to bypass the dollar-denominated SWIFT network should China ever be cut off from SWIFT.

To further enhance RTPs, in 2020 the People’s Bank of China (PBOC) began piloting a central bank digital currency (CBDC) for use domestically. CBDCs offer cheaper, faster, more secure payments and by 2023 transactions had reached USD 249.33 billion, establishing China as leader in the development of digital currencies. Digital wallet providers like WeChat Pay are now expected to begin incorporating CBDCs into their mobile payments platforms.

Concurrently, China is working on an international roll out of its digital yuan. The PBOC is collaborating with the Bank for International Settlements on project mBridge, which aims to develop an interoperable platform for cross border payments using digital currencies. By removing the inefficiencies and cost layers of correspondent banking from the process, CBDCs have the potential to significantly streamline cross border payments to the benefit of businesses and consumers alike.

China’s commitment to a digital economy places the country at the forefront of payments innovation, in addition to being the number one outbound student market. Education institutions that rely on student mobility, must prioritize the advanced expectations of Chinese consumers when it comes to cross border payments for things like tuition, fees and accommodation.

Real time payments flourish in Brazil and India

China’s RTP market might be strong, but India is the undisputed leader with a staggering 129.3 billion transactions in 2023. In second place, Brazil has experienced 228.9% market growth to reach 29.2 million transactions.

Interestingly, major economies such as the US and UK, which make up the top two destinations for international students, are lagging in adoption of real time payments.

India launched its Unified Payments Interface (UPI) in 2016, incorporating instant payments with QR codes and digital wallets, mobile phone numbers and virtual IDs. With real time payments now part of daily life for Indian consumers, the government has its sights set expanding the service globally, with a particular focus on the remittances market.

Over in Brazil, RTPs have exploded since the launch of PIX, a real time payments system developed by the country’s central bank that enables transactions to be completed in under 10 seconds, around the clock. Now fully integrated into popular digital wallets and bank systems, PIX has rapidly expanded to over 150 million users. At a G20 meeting early in 2024, Brazil’s central bank announced plans to take PIX global, making cross border payments faster and cheaper.

The adoption of real-time payments is transforming retail payments in Brazil and India. Increasing demand for real time transactions has been driven by the convenience of digital services and the integration with mobile wallets and digital apps. However, RTPs also help drive financial inclusion, with central banks around the world realizing that instant payments can modernize their financial ecosystem, digitize their economies and contribute to GDP.

Flexibility in a rapidly evolving payments landscape

Advancements in financial technology are having a profound impact on global commerce, with the digital era driving a shift in consumer expectations. China’s CBDC advancements, along with India and Brazil’s successful RTP systems, are great examples of fintech innovations that signal oncoming change in the landscape of education payments. Advancements in RTP are also improving the speed and efficiency of bank transfers, making them more cost-effective and reducing transaction risks.

However, Embedded finance, open banking frameworks, blockchain and the expanding use of digital wallets could also change the way international students interact with their chosen education providers. And as the outbound student market continues to grow, education institutions must consider how they intend to accommodate these changes now, to ensure they’re ready for the future.

Want more insights on the topics shaping the future of cross-border payments? Tune in to Converge, with new episodes every Wednesday.

Plus, register for the Daily Market Update to get the latest currency news and FX analysis from our experts directly to your inbox.