Written by Steven Dooley and Shier Lee Lim

Markets continue to reverse into 2024

Financial markets continued to start 2024 with a clear reversal in the short-term trend with the US’s key Nasdaq index staging its first five-day loss since December 2022 and the US dollar benefiting from the broader market caution.

Overnight, the S&P 500 fell 0.3% while the Nasdaq lost 0.5%.

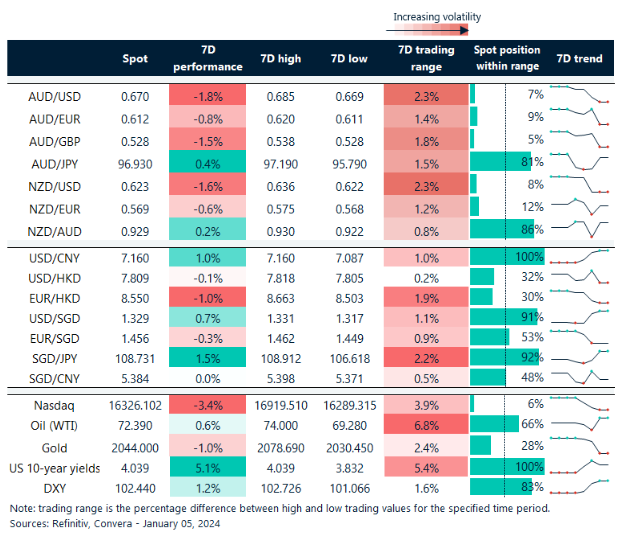

In FX markets, the stronger greenback saw the USD/JPY surge 1.0%. The AUD/USD fell 0.4% while the NZD/USD lost 0.3%.

The USD/CNH climbed 0.2% while the USD/SGD gained 0.1%.

European FX markets were more upbeat, however, after better PMI numbers in Germany, France and the UK. The euro and British pound were both stronger. Eurozone inflation is due tonight.

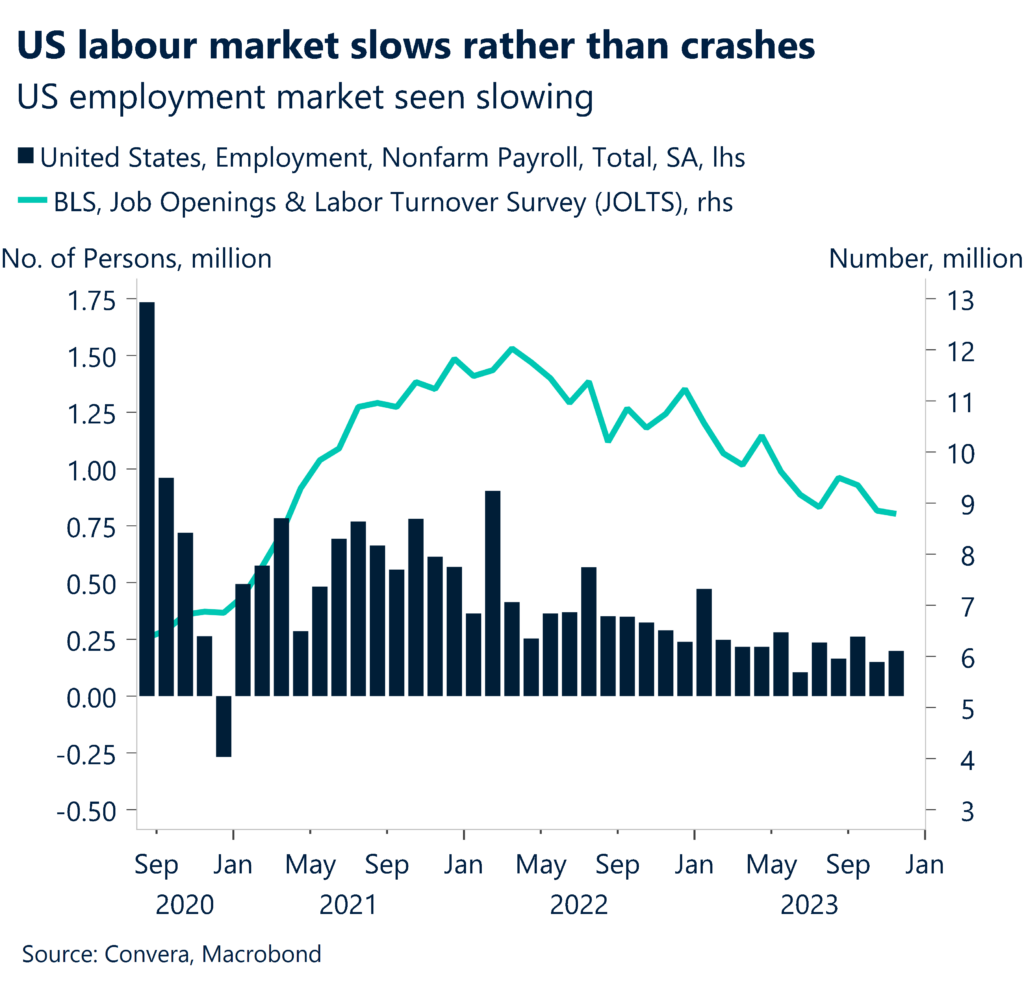

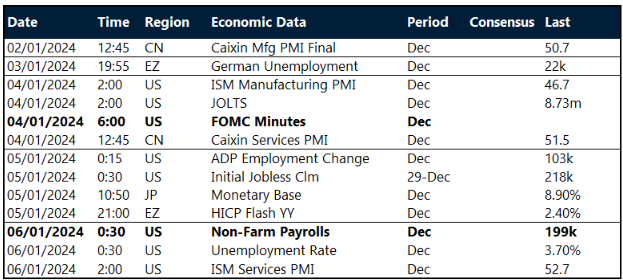

Markets were also more cautious ahead of tonight’s US non-farm employment report. The US labour market has remained strong – last night’s ADP employment reading and weekly unemployment claims both beat expectations – while the NFPs have been stronger than forecast in three of the last four releases.

Tonight, the market is looking for 170k new jobs in December with the unemployment rate forecast to rise from 3.7% to 3.8%. A higher number could drive further USD strength.

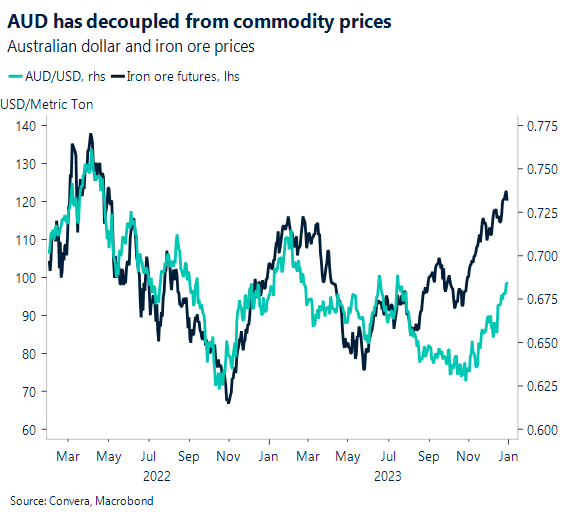

China growth hopes supporting iron ore, Aussie

Iron ore reached 18-month highs this week and the Australian dollar remains the likely winner from any potential China GDP upgrade in 1H24. But for now, the AUD seems more disconnected from iron ore prices.

Since Chinese reflation has mostly relied on commodity-intensive infrastructure and building activity, upgrades to China GDP have historically benefited commodity exporters like ZAR, BRL, and AUD.

However, currencies’ elasticity to further upgrades in Chinese GDP in 2024 is probably going to be less than expected.

Historically, commodities have benefited from China’s GDP boost even in the absence of the housing market support in this cycle. That said, there is doubt over the degree to which hoarding over the previous several quarters has already pushed ahead commodity demand.

Nevertheless, the relative rank order of any China lift is unlikely to shift significantly and suggests a preference for AUD.

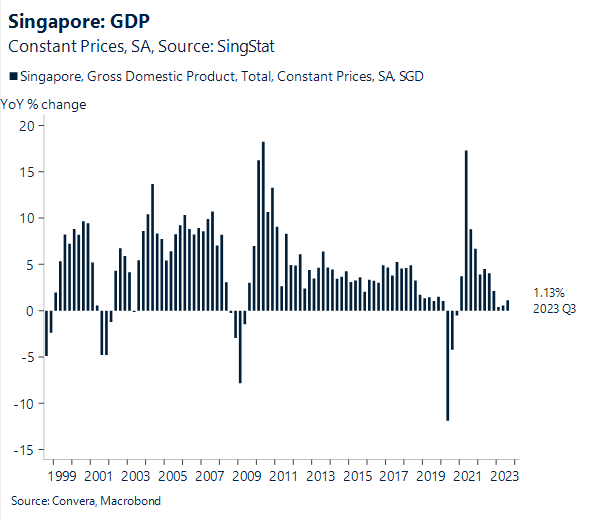

SGD NEER near peak?

Looking forward, 2024 is probably when SGD NEER (nominal effective exchange rate) will peak. Given that Monetary Authority of Singapore looks likely to have completed its tightening cycle and pricing pressures in the city state are continuing to show signs of moderating, a lower rather than a higher SGD NEER is probably in store for the next big shift.

Given its present position +190bps above the midpoint and the 150bps slope of the bands, the SGD NEER’s tendency to migrate towards the midpoint late in the economic cycle may restrict its performance.

Because of its generally low beta, the SGD is therefore expected to follow the wider USD, but when the business cycle flips, we see that the risk-reward will start to tilt in favour of being negative on SGD.

Aussie, kiwi fall to seven-day lows

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 1 – 6 January

All times AEDT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.