US indices rallied on Tuesday as easing AI concerns sparked a broad recovery, lifting the S&P 500, Nasdaq 100, and Russell 2000 despite weakness in energy and healthcare. While Alphabet was the only “Magnificent 7” member to finish in the red, Bitcoin stabilized after an early dip below $63,000. All eyes now turn to AI bellwether Nvidia, which is set to report quarterly results after today’s closing bell.

CAD: Behind a narrow trading range

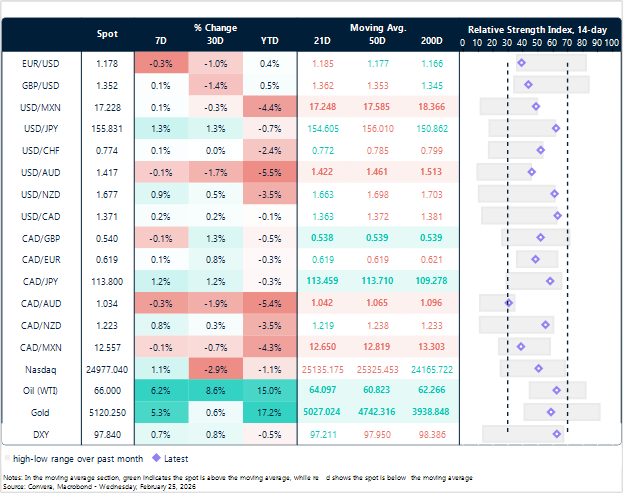

When viewed over a three-year horizon, the CAD sits at just 17% of its 12-month range and 39% of its 36-month range. While the 1.35 to 1.45 corridor has defined price action over the last three years, the trading range has narrowed significantly since volatility subsided last April. This compression reflects a stagnant macro outlook and a lack of movement in yield differentials relative to the US.

Since “Liberation-day,” the Loonie has capitalized on a significant 8.8% rally against the Japanese yen and a 4.4% gain against the US dollar, yet it remains a notable laggard among its commodity-linked peers. This relative underperformance, particularly against the Australian dollar and Swiss franc, stems from a cooling of economic momentum following the end of 2025 and persistent geopolitical friction with the United States. While an expansionary budget and ample monetary stimulus provide a theoretical floor for the currency, it remains caught between USD’s status as a beneficiary of safe-haven rotations and the heavy weight of regional trade uncertainties.

The internal economic landscape further complicates the bullish narrative, specifically regarding the Bank of Canada’s path after trimming rates to 2.25%. While some market observers suggest the easing cycle has concluded, the looming “mortgage renewal wave” represents a massive, unpriced risk that could force the central bank to diverge from the Federal Reserve. With approximately 60% of outstanding mortgages set to reset by the end of 2026, many facing payment hikes of 15% to 20%, the resulting debt-service shock threatens to suppress domestic demand far more than headline employment data suggests. Recent labor reports highlight this underlying fragility, as a lower unemployment rate has been offset by stagnant wages and a growing dependency on public-sector hiring. If this consumption squeeze intensifies, the widening interest rate gap in favor of the US dollar will likely prevent the CAD from sustaining any significant rally.

Structural hurdles and the looming CUSMA 2026 joint review add a persistent risk premium that discourages the long-term foreign investment needed for a broad-based recovery. Canada’s labor productivity continues to trail US levels significantly, and the retreat of Canadian travelers from international trips suggests that recent domestic spending trends are a symptom of decimated purchasing power rather than economic vigor. From a valuation perspective, while metrics like the Big Mac Index hint at a theoretical undervaluation toward 1.25, the Real Effective Exchange Rate more accurately reflects the current 1.37 spot as a fair representation of these structural constraints. Until there is a formal trade truce with the US or a definitive reversal in productivity trends, the Canadian dollar is expected to remain range-bound between 1.35 and 1.43, as the market balances long-term value against the immediate reality of a highly leveraged domestic consumer.

USD: DXY’s attempt at the 98 mark

The US dollar index (DXY) remains capped by its 50‑day moving average (97.940), which sits near the 98 mark – a level the index has failed to reclaim since USD sentiment soured in early January 2026. Supported by a spike in oil prices and a hawkish‑leaning Federal Reserve that welcomes signs of a more stable labour market, the dollar has staged a comeback from its January lows at 95.551, levels last seen in 2022. Yet for a move above 1.18, investors appear to be waiting for further developments on the trade front. In yesterday’s State of the Union address, Trump reiterated his resolve to impose trade tariffs despite the SCOTUS ruling, leaving the dollar to start today’s session on the soft side.

Even so, the dollar so far appears largely unbothered by the uncertainty unleashed by the SCOTUS ruling on tariffs. Markets may be leaning toward a scenario where the eventual tariff rate ends up lower. But as we saw in 2025, the path to the tariff outcome can matter more for the dollar than the final rate itself. Reliance on alternative tariff mechanisms – potentially narrower in scope and less durable than those struck down – could create an even more uncertain environment, something investors are unlikely to welcome.

Onto the Fed outlook, we heard from several FOMC members yesterday – Governor Lisa Cook, Chicago Fed President Austan Goolsbee, and Governor Christopher Waller. Their messaging was broadly aliged: the focus is shifting more unanimously toward the inflation outlook, with the labour market showing clearer signs of stabilisation. Markets have taken note, with no meaningful rate cuts priced before July.

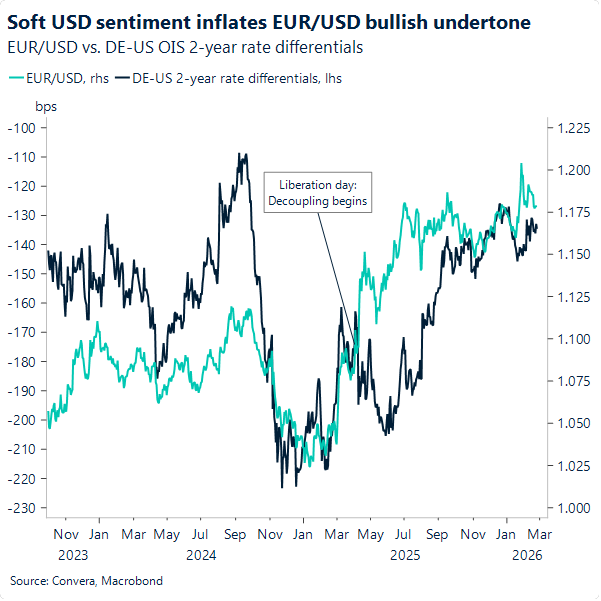

EUR: EUR/USD holds the line

EUR/USD has glided along the 50‑day moving average since last week (1.1774), with its slope – and that of other key averages – essentially flat, offering little directional bias as the pair waits for its next catalyst. As we’ve noted repeatedly, a return to a 1.15–1.18 range would be understandable, but we’re not convinced the balance of risks favours that setup just yet. Bullish fuel from the Fed’s hawkish leanings remains muted by lingering soft USD sentiment. While the former is getting the data it needs to firm up, the latter has grown more vulnerable to further deterioration following the SCOTUS ruling on Trump’s tariffs. Yet markets appear to be waiting for additional clarity before folding this development into the USD‑negative narrative outright and pushing EUR/USD firmly back above 1.18. In the meantime, we read the patient drift just above the 50‑day as a sensible technical posture ahead of clearer direction returning to price action.

MXN: Mexico growth revisions bolster strong Peso

The Mexican economy finished 2025 with far more vigor than initially reported as significant upward revisions showed a 0.9% QoQ growth rate in the final quarter. While the 0.6% annual expansion was lower than the 1.4% recorded in 2024, the momentum is undeniable after Q3 was revised from a contraction to a 0.1% gain. December economic activity proved particularly resilient by jumping 3.3% YoY and 0.4% MoM, prompting analysts to hike their 2026 growth expectations to 1.7%. This strength suggests that the typical dip seen during a first year in office was largely avoided thanks to cabinet stability and a steady fiscal hand.

These robust figures surprisingly provide a green light for Banxico to begin easing policy as early as March with a 25-basis point cut. Even though the Feb bi-weekly headline inflation print of 3.92% was slightly warm, the core reading cooled to 4.5% which remains the central bank primary focus. The combination of a stable currency and a widening output gap means the 11.00% interest rate from last year is likely headed toward a 6.25% terminal level by June 2026. Banxico is expected to prioritize these improving price dynamics while the economy maintains enough self-sustaining energy to handle a gradual return to neutral territory.

The Mexican Peso continues to dominate the FX global stage with a 4% rally YTD as it captures the best of both worlds. High real yields combined with a growth forecast that targets 2.3% by 2027 make the currency one of the leaders of the emerging market carry trade. Investors are betting that a recovering global manufacturing cycle and artificial intelligence related investment in the US will keep the MXN buoyed regardless of short-term volatility. With a massive infrastructure plan on the horizon for 2027, the long-term outlook remains bright for the currency as it stays at the top of the performance charts.

Market snapshot

Table: Currency trends, trading ranges & technical indicators

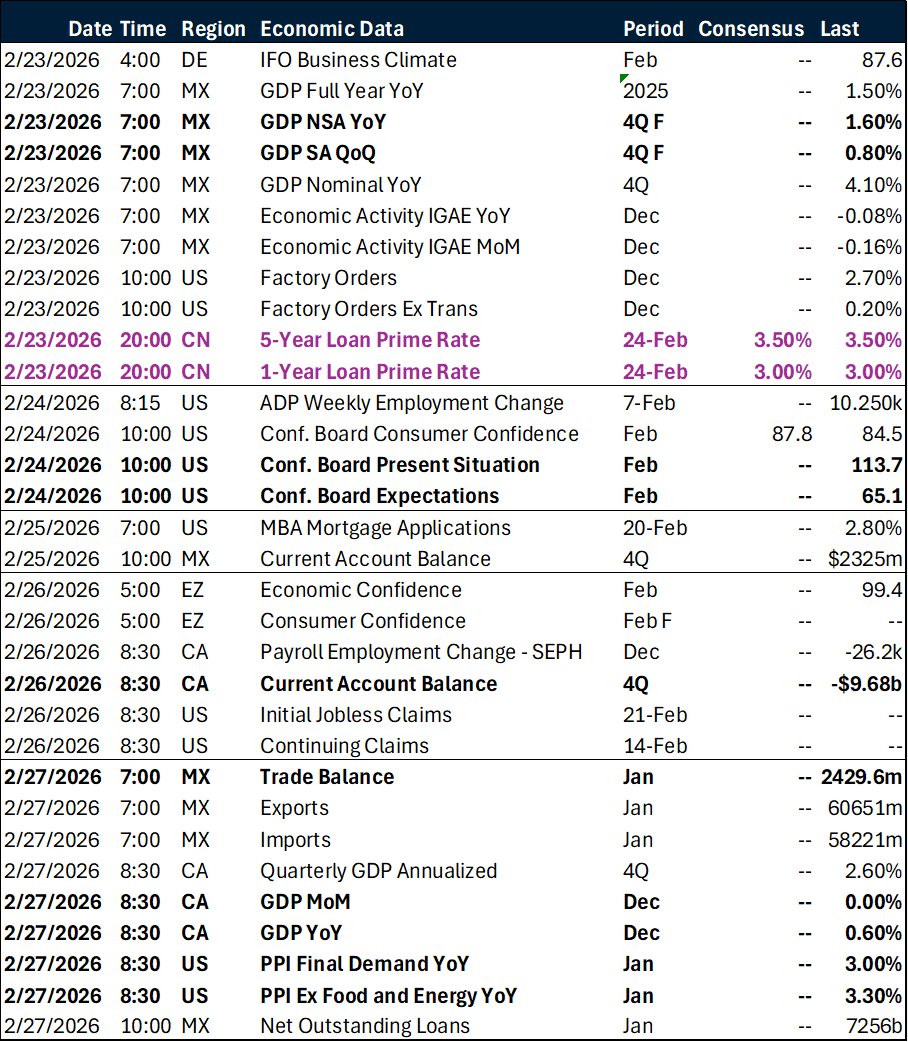

Key global risk events

Calendar: February 23 – 27

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.