USD: Greenback holds the high ground

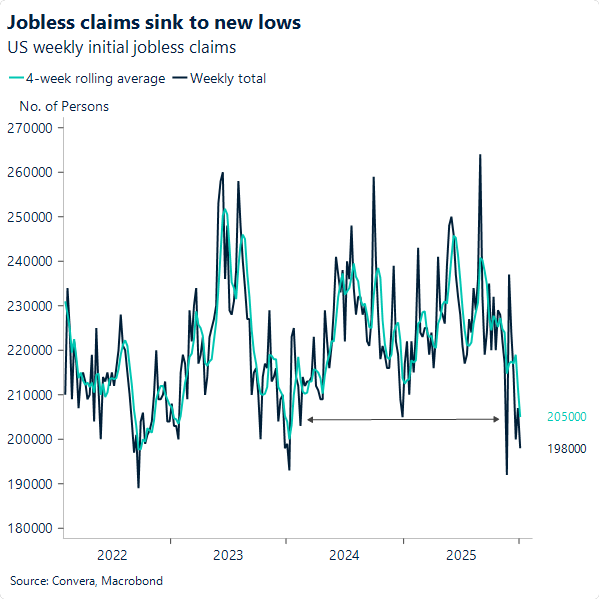

The Beige Book released on Wednesday, which painted a picture of solid economic activity alongside a soft but stable labour market, may have gained more data‑driven texture after yesterday’s weekly jobless claims came in below expectations. The four‑week moving average declined by 6.5k to 205k, the lowest level in two years.

In the face of data that has failed to challenge the Fed’s hesitant easing stance, the dollar index has managed to maintain its bullish structure this week, securing higher highs and higher lows, and was tested yesterday by resistance at 99.500.

We also believe that the firm stance taken by Powell earlier in the week regarding the DoJ’s criminal investigation, combined with broad‑based support from key political figures in the US government and central bankers globally, helped extract much of the political risk premium from the dollar’s price action. If anything, it provided an element of support to the greenback by reaffirming the Bank’s independence amid hawkish data signals, pointing to a path of least resistance in holding rates for now.

EUR: Euro softens as consolidation deepens

EUR/USD heads into the end of the week 0.3% lower and down 1.3% on a month‑to‑date basis. It is not the sort of weekly performance many had anticipated following Monday’s renewed Fed independence threats, which markets appear to have taken in stride.

Meanwhile, a retreat from December’s dollar‑negative seasonality, which saw the pair approach highs near 1.18, is taking shape. These seasonal patterns have partially fed the recent choppy price action and reinforce the broader consolidation the pair has been stuck in for months.

EUR/USD now trades closer to the 200‑day moving average at 1.1587 than at any point since early 2025. This proximity reflects EUR/USD’s hesitant tone, and a break below it would imply a bolder exploration of the 1.15 area.

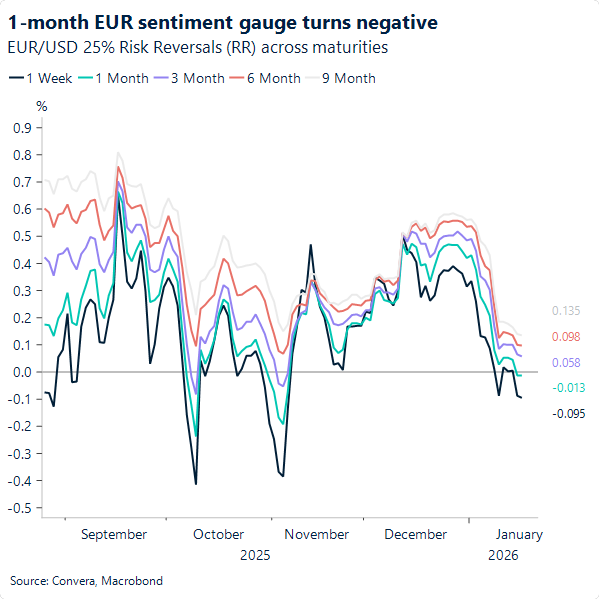

This technical setup warrants a meaningul shift in positioning, as suggested by the options market. 1‑month EUR/USD risk reversals – a key positioning gauge – have turned bearish for the first time in more than two months. This indicates that, until now, traders had been paying more for call options that bet on a stronger euro than for puts that hedge against downside risk. The gauge moved into negative territory yesterday, signalling a bearish directional bias embedded in EUR/USD price action over the coming month.

GBP: The puzzle of a positive day that didn’t deliver

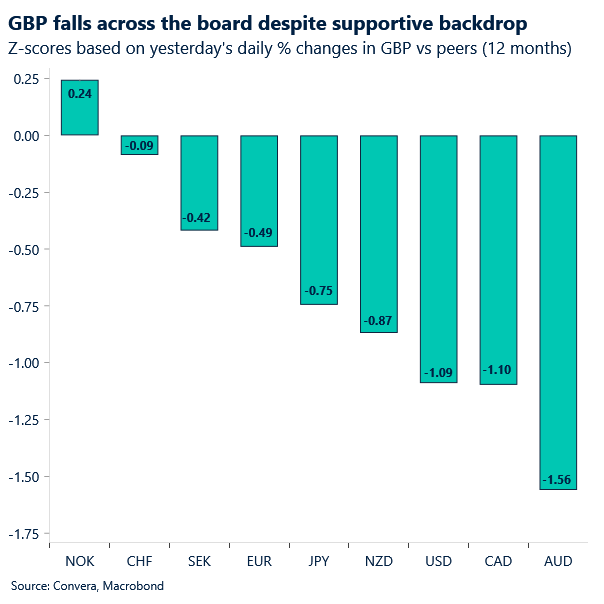

Yesterday delivered one of those market head‑scratchers: sterling weakened broadly despite a backdrop that looked tailor‑made for GBP strength. On paper, Thursday should have been a solid day for sterling — in reality, the UK currency suffered its biggest daily loss in several weeks versus major peers.

The underlying conditions looked firmly GBP‑positive. Risk sentiment improved: equities were higher, volatility gauges like MOVE and VIX drifted lower. Oil prices sank over 4%, which would typically support GBP by easing the UK’s energy‑import burden. Even gilt yields rose as markets trimmed BoE easing expectations after a stronger‑than‑expected UK GDP report. Yet the pound still underperformed — and that’s the tell.

As we’ve highlighted this week, sterling is now reacting more aggressively to USD swings than other major peers, a dynamic that has steadily intensified over recent months. And that relative underperformance naturally feeds into the crosses. It’s a flow‑driven dynamic rather than a fundamental one.

GBP/USD posted its biggest daily fall since November. That said, when -0.4% counts as a standout move, you know FX volatility is running on empty. In the near term, any further USD strength will naturally drag GBP/USD lower: the 100‑day moving average at $1.3366 is acting as key support, and a break below it would open the door to a move toward $1.33. All of this sets the stage for a data‑packed week ahead for the UK, where fresh catalysts could finally jolt sterling out of its low‑volatility drift.

Market snapshot

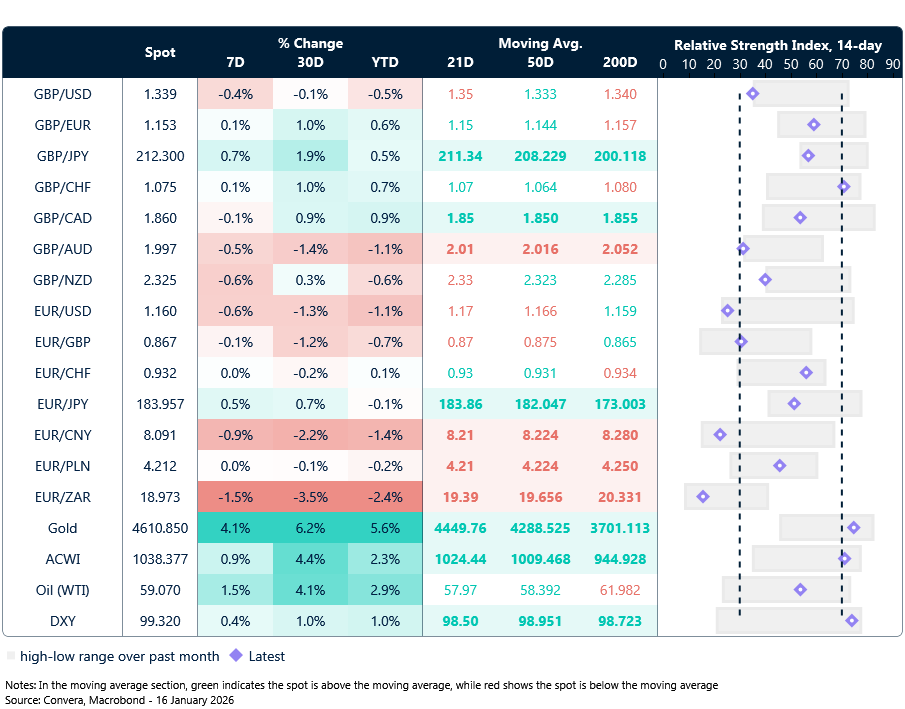

Table: Currency trends, trading ranges & technical indicators

Key global risk events

Calendar: January 12-16

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.