USD: Dollar stumbles as trade risks multiply

Despite somewhat appeasing words from President Trump yesterday – “we will probably be able to work something out” – that may certainly help contain further important losses in the dollar today, we remain at peak trade tensions. This time, markets are facing a far more confrontational Europe, adopting something closer to a China‑style approach, and the shift is rattling sentiment. Equities retreated while high‑beta currencies took the brunt of the move. We are hearing mind‑boggling threats of a 200% tariff on France’s champagne imports – something markets might have taken in stride had it not been paired with immediate retaliatory action from Europe. The VIX briefly pushed above 20 for the first time since November, suggesting markets may no longer be willing to shrug off geopolitics as much as they were earlier this month.

Add to this an imminent Supreme Court ruling that may deem Trump’s tariffs illegal, the nomination of the next Fed chair – almost certainly a dove – and the still‑fresh escalation of intervention in Fed affairs via the DoJ’s legal route, and the dollar is trembling on reignited “sell‑America” fears, having fractured a bullish setup that saw the dollar index riding above all key moving averages, now piercing back through the 98 zone. In other words, while the bar was high for further dollar weakness on this front, when you get a confluence of de‑dollarisation themes coupled with Europe’s retaliatory stance, market calmness begins to crack.

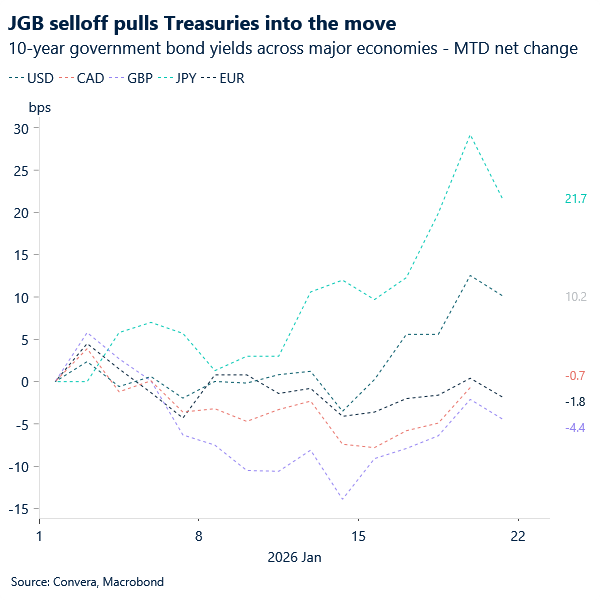

Coincidentally, bonds sold off in Japan, where Prime Minister Takaichi official called for an early snap election on February 8 aimed at shoring up her ruling party’s narrow coalition majority. The announcement heightened concern that it may pave the way for looser government spending that exacerbates the nation’s already fragile finances while adding fuel to still‑elevated inflation. JGB long‑end yields jumped to their highest levels in decades. Treasuries followed, a typical cross‑market contagion move that was nonetheless justified by domestically driven factors, compounding dollar bearishness.

However, overnight, we saw JGBs rebound, and Treasuries followed, stripping away a bearish catalyst from what is likely to be a calmer day for the dollar as markets await further developments before committing to a more defined view of sharp USD selling.

One thing to note here is that while sell‑America fears inevitably made a comeback, sending the dollar 0.8% lower week-to-date, these are unlikely to resemble the 2025 post‑Liberation Day episode. Investors are now far better USD‑hedged compared with the highly unhedged 2025 environment that warranted heavy dollar selling. Also, there is still an inclination to look through these geopolitical flare‑ups and lean on the resilient US macro story to justify a more orderly dollar profile at the start of 2026, yet markets are waiting for further updates before challenging, or re-embracing, that narrative with greater conviction.

CAD: Still clouded by tariffs

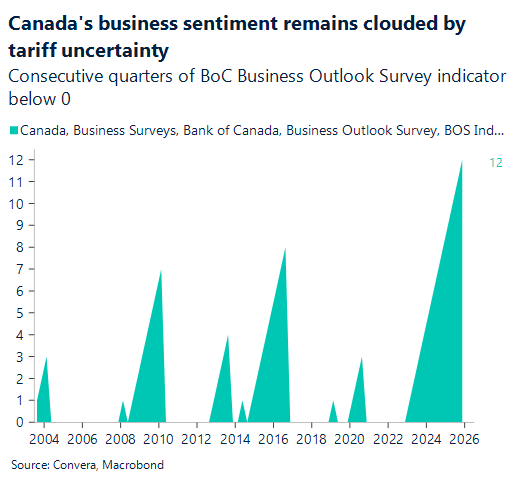

This week the Bank of Canada released its Canadian Survey of Consumer Expectations and Business Outlook Survey for the fourth quarter of 2025, and the outlook is pretty grim: households are feeling the squeeze, with financial sentiment stuck well below pre-pandemic norms. People are stressed about missing debt payments and losing their jobs, leading to a major pullback in spending as they hunker down and wait for the other shoe to drop on trade conflicts. Even though long-term inflation fears are cooling off, the immediate reality of high prices and tariff-driven uncertainty has Canadians playing it safe, trading international vacations for domestic ones and aggressively hunting for “Made in Canada” labels.

This consumer-level anxiety is hitting corporate Canada hard, as the Business Outlook Survey shows business sentiment is equally subdued and struggling to claw back from recent lows. Companies are reporting weak sales growth thanks to the same trade tensions weighing on households, and while they’re hoping for a slight turnaround, most are just maintaining their current staff and sticking to routine maintenance instead of making big expansion bets. It’s a bit of a stalemate; firms have plenty of capacity and can find workers easily because demand is so soft, and until the uncertainty around U.S. trade policy clears up, both businesses and consumers seem stuck in a cautious, defensive holding pattern.

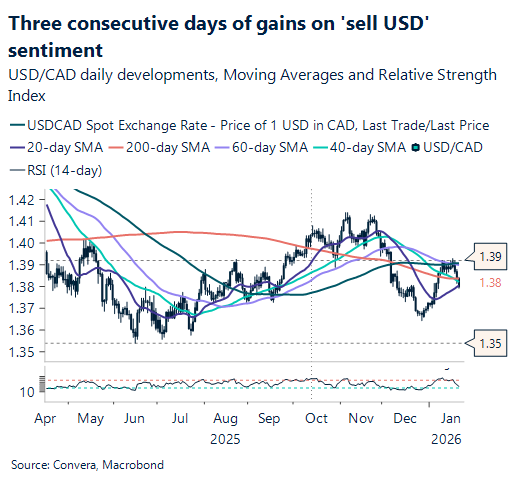

In FX, it’s 3 consecutive days of gains for the USD/CAD. With the moving averages now flattening out, the USDCAD is poised to continue range bound. The primary resistance is firmly established between 1.3870 and 1.3900, a zone reinforced by the 50-day moving average and the base of the Ichimoku cloud, which continues to cap any attempted rallies. On the downside, the market is finding a reliable floor near the 1.3750 to 1.3780 area. Until we see a high-volume breakout beyond either of these levels, the pair is likely to continue its “ping-pong” price action, treating these horizontal zones as the definitive boundaries for the near term.

MXN: LatAm as tariff hedge?

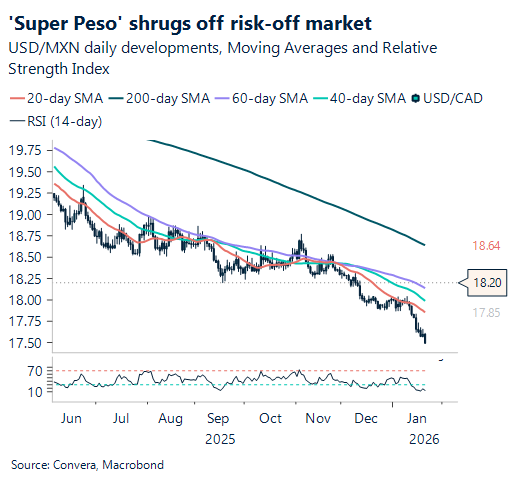

While developed markets grapple with a fresh wave of geopolitical “noise” and trade uncertainty, the Mexican Peso has emerged as a standout performer, defying the broader risk-off sentiment. The currency has rallied to its strongest level in over a year, trading near the 17.60 mark. This resilience is particularly striking given the turmoil in the U.S. and Europe, where new tariff threats, have sparked a “sell America” trade. For the Peso, the narrative has shifted from being a victim of trade wars to a beneficiary of high-interest-rate differentials and a perceived ceiling on U.S. dollar strength, bolstered by Banxico’s restrictive 7% policy rate and the continued tailwind of nearshoring.

However, this “shining” performance has made the trade increasingly crowded, triggering a significant warning from JP Morgan. The bank downgraded its view on emerging market currencies from “overweight” to “market weight,” explicitly warning that the market has become “overbought” following its year-long rally. Their internal EM FX Risk Appetite Index has moved into territory that historically triggers a “sell signal,” suggesting that much of the optimism regarding high yields and tariff-hedging may already be priced into the Peso. JP Morgan noted that while structural tailwinds remain, the sheer volume of capital that has flooded into EM assets—driven by a 10% drop in the U.S. dollar—creates a tactical risk of a sharp reversal.

Ultimately, the Mexican Peso sits at a volatile crossroads where fundamental strength meets technical exhaustion. While Latin American equities have surged 6.4% year-to-date, significantly outperforming their developed-market peers, the “Super Peso” is now facing its toughest test of 2026. The cooling sentiment from institutional heavyweights serves as a reminder that the very strength making the Peso a standout can also be its Achilles’ heel; if global volatility continues to rise, the overcrowding of this popular trade could lead to a sudden liquidity squeeze. For investors, the challenge is now distinguishing between a structural shift toward emerging markets and a tactical bubble that is ripe for profit-taking.

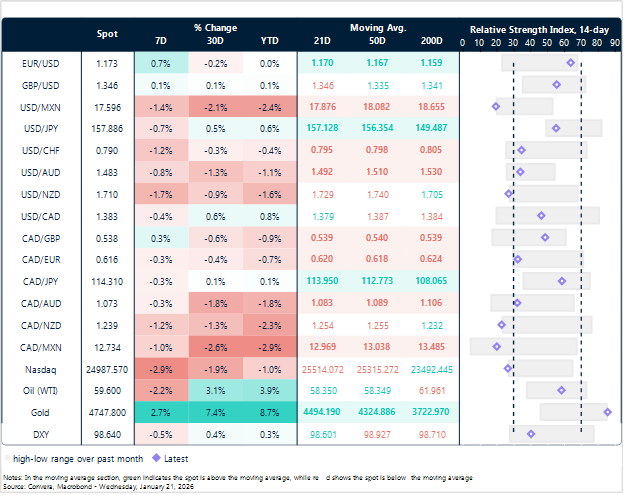

Market snapshot

Table: Currency trends, trading ranges & technical indicators

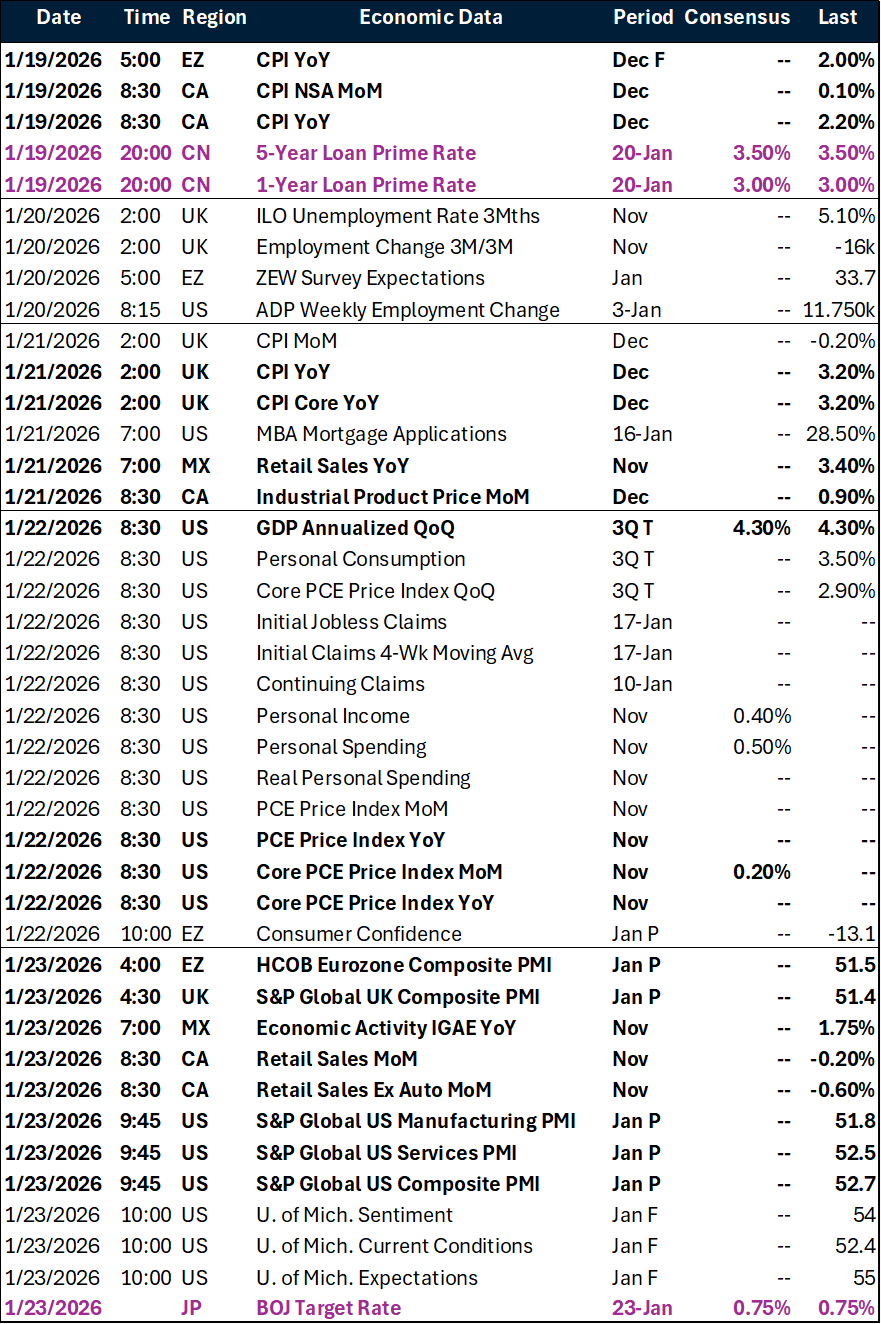

Key global risk events

Calendar: January 19-23

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.