Tech slump and bond surge set the tone before US CPI

US Treasuries rallied sharply, with 10-year yields dropping ~7.5bps to 4.10%—the lowest since mid-December—as short covering intensified and risk assets sold off.

Nasdaq tumbled 2%, S&P 500 fell 1.5%, and tech names like Apple (-5.5%) and Cisco (-12%) led declines amid renewed AI competition fears.

Jobless claims edged down to 227k, but existing home sales slumped 8.4% to their lowest since September 2024.

UK gilts outperformed after Q4 GDP missed expectations (+0.1% q/q vs. +0.2% consensus), reinforcing the case for BoE easing. Policymakers flagged that inflation is on track for target, and a further rate cut by April is seen as “reasonable.”

The RICs house price balance improved to -10% in January, the best since June 2025.

Aussie bonds lagged as RBA officials struck a hawkish tone, warning further hikes remain possible if inflation persists. Consumer inflation expectations jumped to 5% in February.

Trump flagged a positive US-China relationship, with reciprocal visits planned for April and later in the year, keeping geopolitical risk in check as Asia opens.

All eyes now turn to tomorrow’s US CPI print, with consensus looking for a 0.3% m/m core rise and 2.5% y/y.

AUD/USD down 0.5% and Kiwi down 0.2% overnight on risk-off mode.

USD/SGD was flat and USD/CNH was down 0.2%.

Dollar index held steady near 97.00 handle.

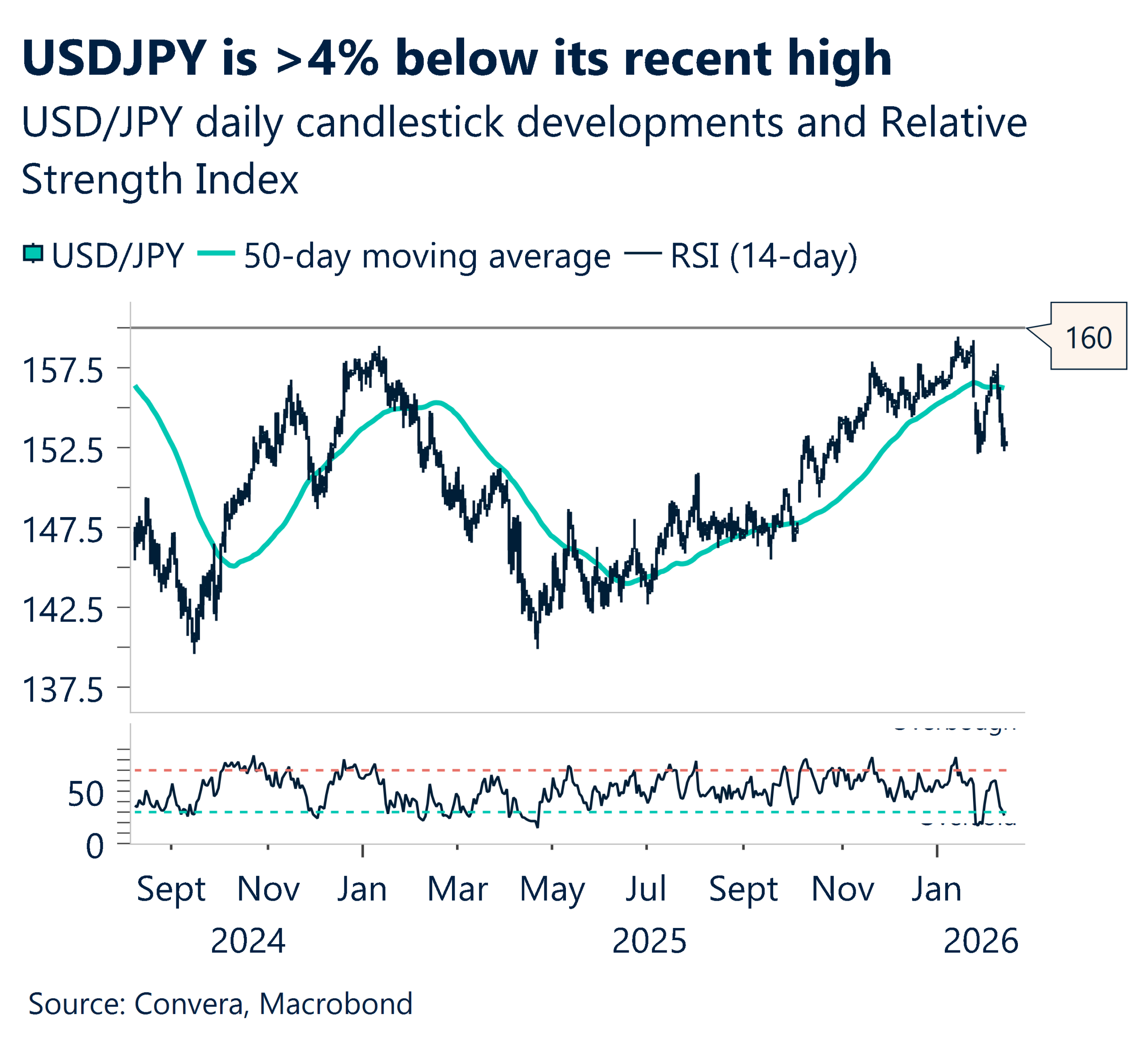

Japan steps up watch, USDJPY down 4% from peak

Japan’s top currency official, Masato Mimura, said he is watching currency moves closely and with urgency, noting that Tokyo remains in steady contact with US counterparts.

The yen has strengthened even after the LDP’s sweeping election win, pushing back against the so‑called “Takaichi trade” narrative.

USD/JPY has dropped more than 4% from its recent peak of 159.45, last reached on January 14. The next key levels to watch sit near the 100‑day average at 154.33 and the 21‑day average at 155.23.

Fed voices lean toward holding steady

Cleveland Fed President Beth Hammack said January’s jobs report shows unemployment stabilising, suggesting the labour market is settling into what she called a “healthy balance.” She warned that inflation is still too high and that interest rates may stay on hold for longer.

Dallas Fed President Lorie Logan also backed keeping rates unchanged unless the labour market shows clear new weakness. Kansas City Fed President Jeff Schmid echoed that view, saying rates should remain “somewhat restrictive” with growth still firm and inflation elevated.

In contrast, Fed Governor Stephen Miran struck a more dovish tone, arguing that there is room to consider rate cuts even after the stronger‑than‑expected January jobs report. He said that continued improvements in the supply side of the economy give policymakers space to accommodate.

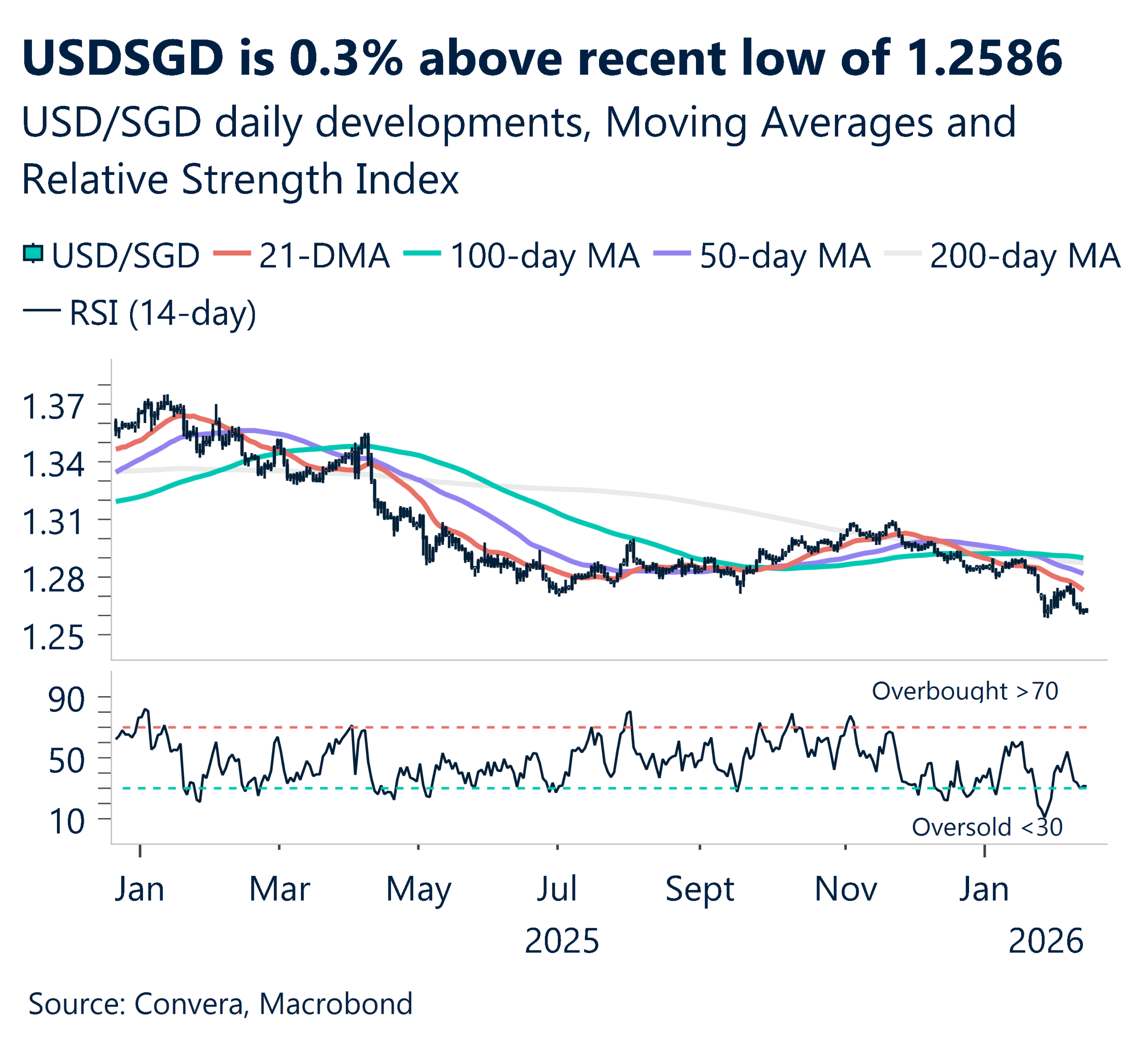

Across Asia, USD/SGD pair is trading about 0.3% above its recent low of 1.2586, last reached on January 28. The next levels to watch sit near the 21‑day average at 1.2710 and the 50‑day average at 1.2788.

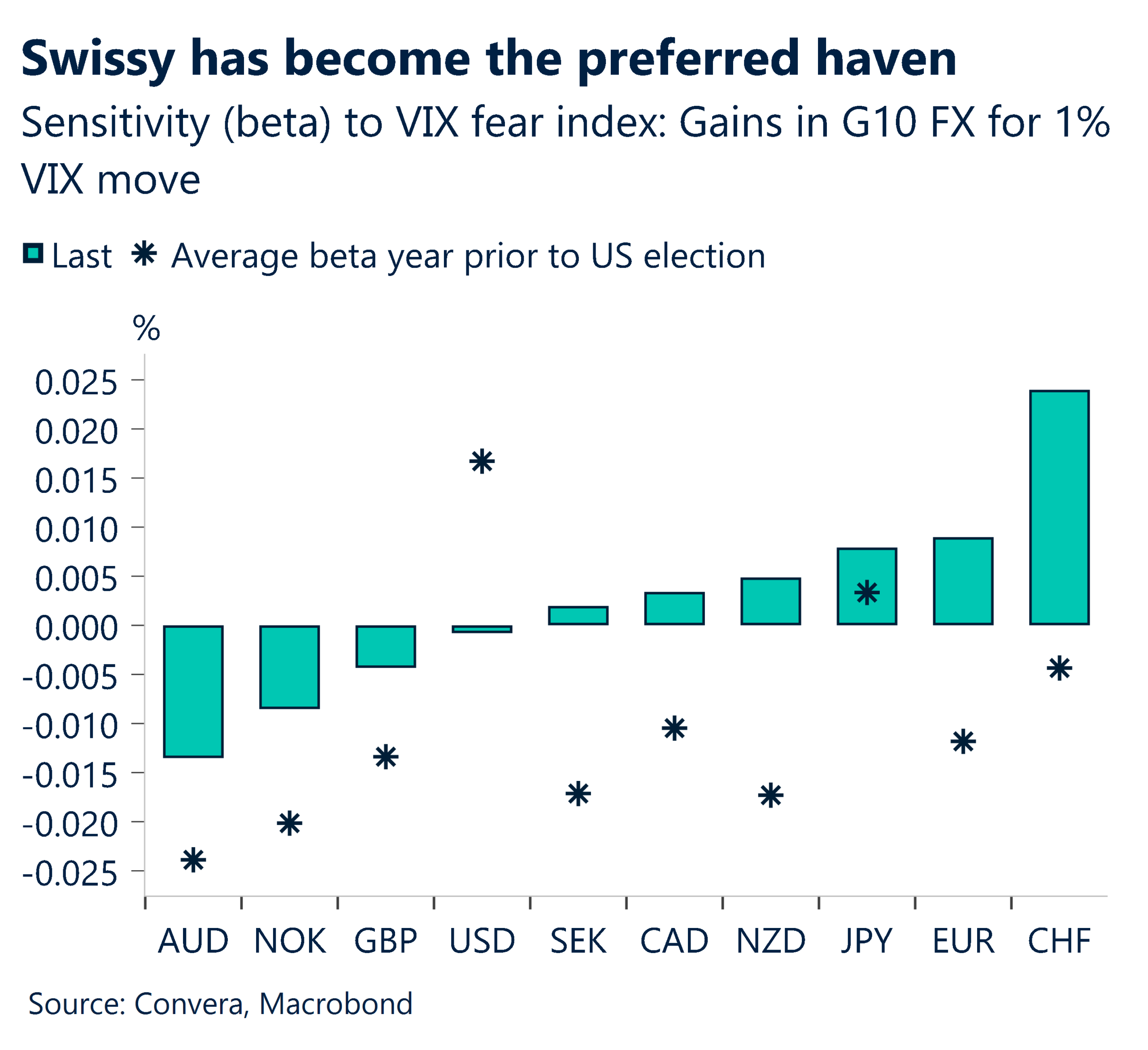

Antipodeans down on risk off

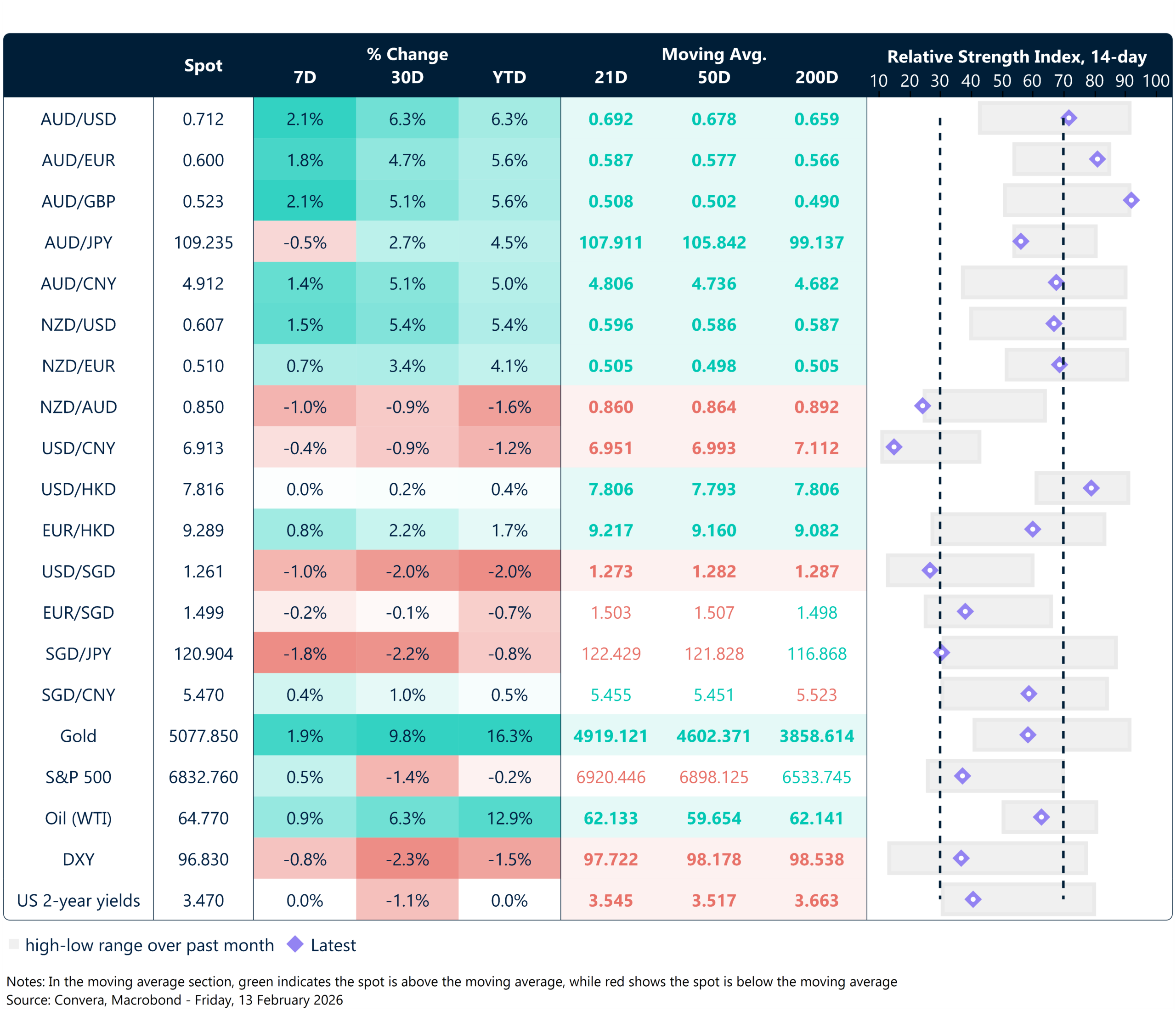

Table: seven-day rolling currency trends and trading ranges

Key global risk events

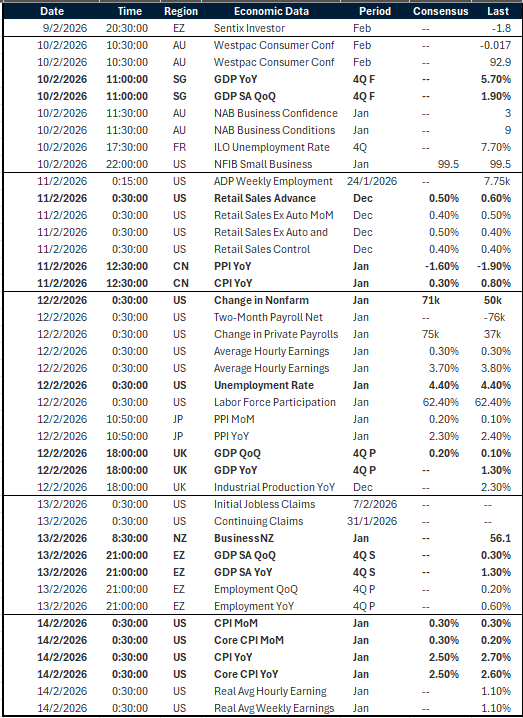

Calendar: 9 – 14 February

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.