Written by Steven Dooley, Head of Market Insights, and Shier Lee Lim, Lead FX and Macro Strategist

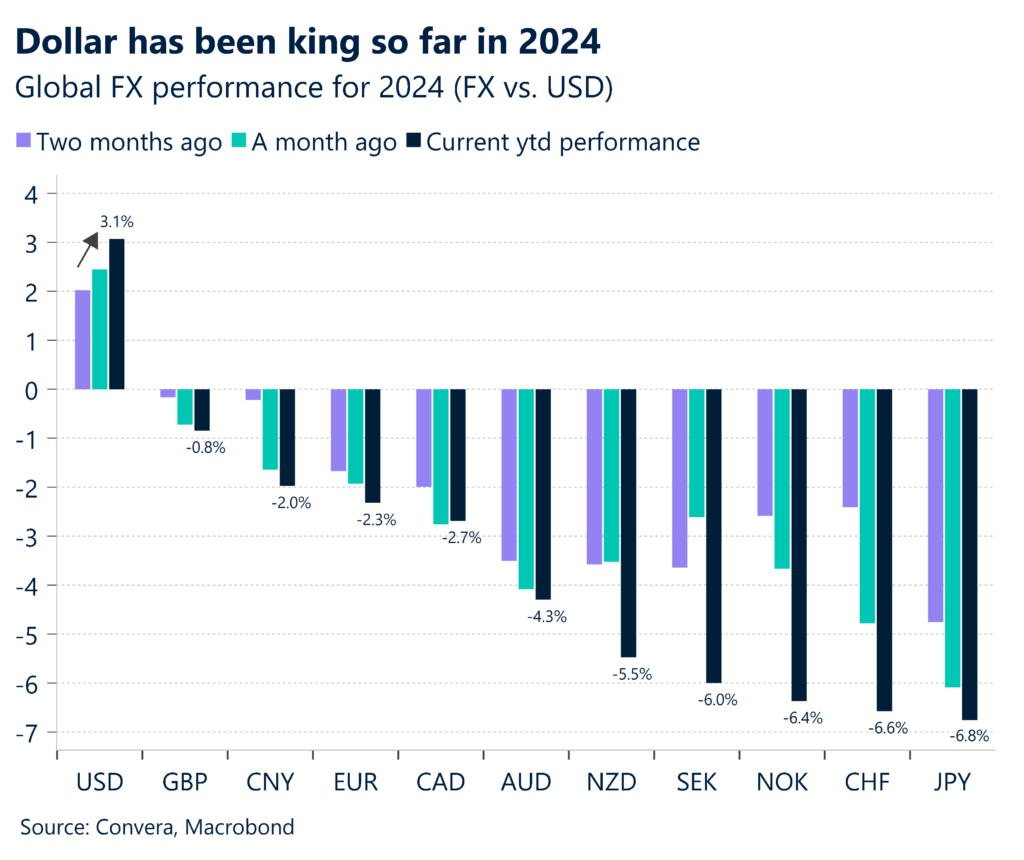

Greenback reverses as shares fall

The US dollar reversed from five-month highs overnight, with US shares lower driven by worries the US Federal Reserve might need to delay rate cuts due to a booming US economy.

US bond yields jumped to the highest level since November with the benchmark 10-year bond yield ending at 4.36% overnight – up from 3.78% at the start of the year. The US’s Dow Jones index fell 1.0% overnight.

The US dollar’s fall even as US bond yields climbed overnight provides some evidence that much for the USD’s recent strength is due to the US economy’s growth potential – not just interest rate differentials.

The US dollar was weaker in most markets. The USD/JPY fell 0.1%, GBP/USD gained 0.2% and EUR/USD climbed 0.3%.

Across the region, the AUD/USD gained 0.3%, NZD/USD was up 0.3%, USD/SGD fell 0.1% while USD/CNH was flat.

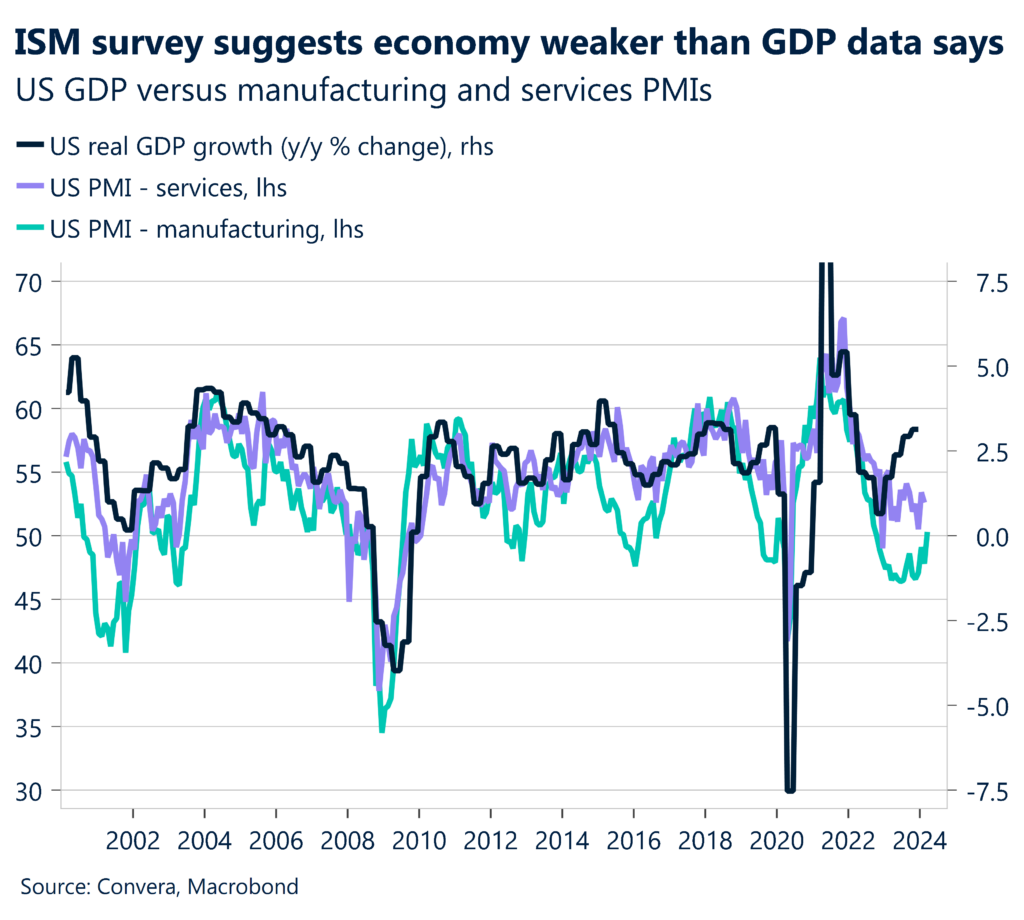

A stronger ISM manufacturing survey, released Monday, was the major driver for the reversal in markets this week. Tonight, the ISM services survey is released.

Mixed signals for USD from services data

After an ongoing run of better performance from US data, markets are looking for an increase in ISM services from 52.6 in February to 53.0 in March when the survey is released at 1.00am AEDT on Thursday.

While recent NY Fed and KC Fed surveys saw a significant gain, the Philly Fed and Dallas Fed services surveys saw a dip.

More broadly, the service sector had a general improvement throughout the month, driven mostly by gains in the IT and agriculture sectors. The employment subcomponent most likely increased as a result of fewer layoffs.

Federal Reserve chair Jerome Powell has remained mostly dovish; but this does not remove the higher-for-longer risks which are still dependent on data. Markets looked to become more aware of those risks overnight.

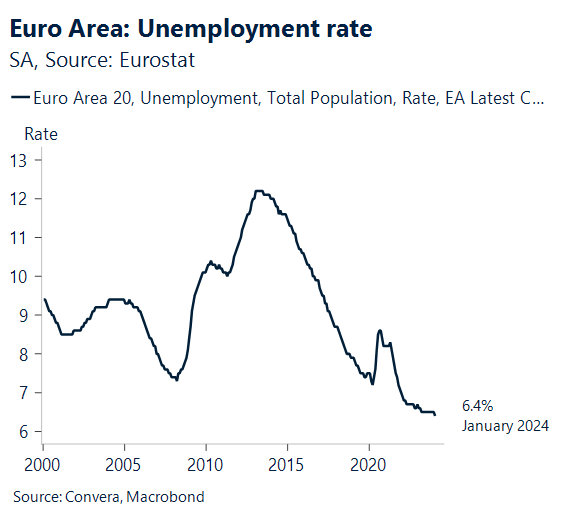

Euro slips ahead of employment

In February, we’re looking for the Eurozone 6.4% unemployment rate to remain steady. There isn’t much proof that the labour market has significantly weakened in recent months.

The number of employed people has increased steadily, industry hours worked have been steady, and the unemployment rate is still significantly higher than it was before the epidemic. Despite the moderately better performance from Eurozone employment – it has missed expectations only once in the last 12 months – a recent bout of euro weakness has seen the AUD/EUR near two-month highs and EUR/SGD at six-week lows.

US dollar index turns near 105 resistance

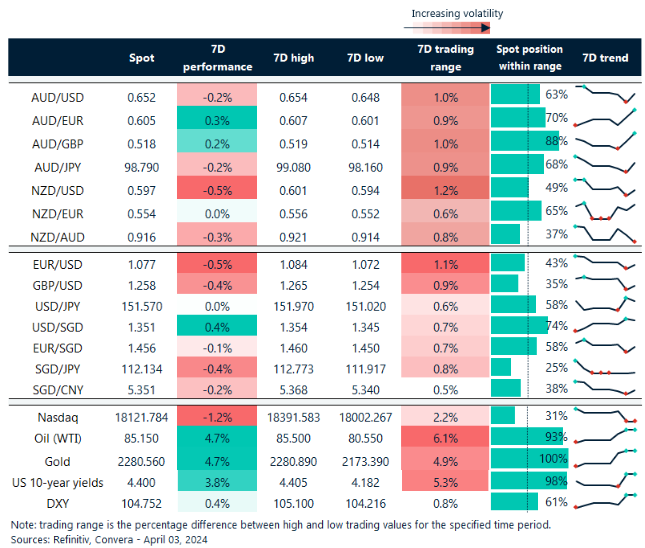

Table: seven-day rolling currency trends and trading ranges

Key global risk events

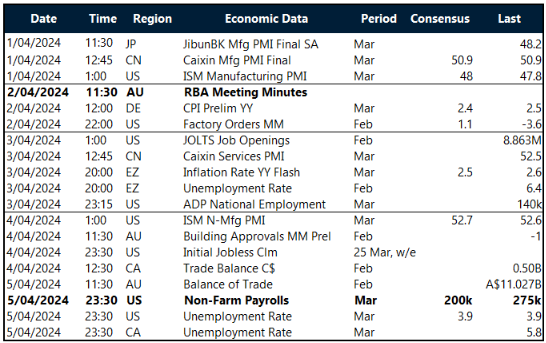

Calendar: 1 – 5 April

All times AEDT

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Have a question? [email protected]

Take a deep dive into the trends shaping cross-border payments with our podcast, Converge.