Written by Convera’s Market Insights team

Upside surprises in core inflation

George Vessey – Lead FX Strategist

The US dollar index (DXY) rose to a 1-week high and Treasury yields bounced from 2-year lows as yesterday’s US inflation report raised bets the Federal Reserve (Fed) will opt for a 25-basis point rate cut rather than a 50-basis point cut next week.

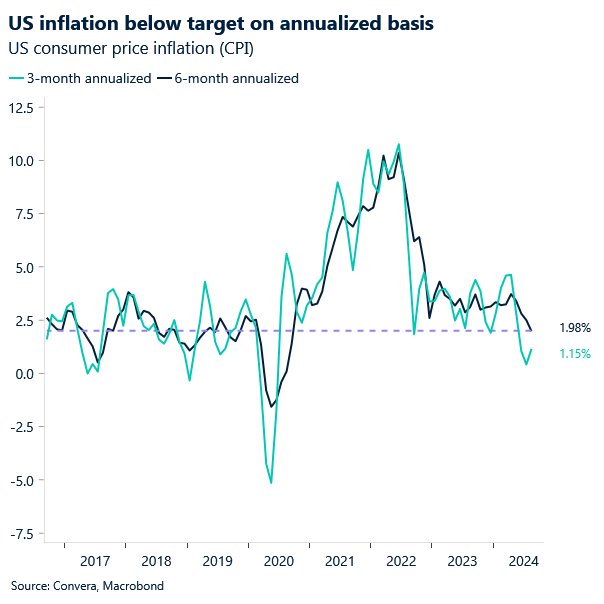

The CPI report was the last big data release amidst the blackout period before the much-anticipated Fed meeting. The headline rate slowed for a fifth consecutive month to 2.5% in August, the lowest since February 2021 and the six-month annualized CPI measure dropped below 2% for the first time since 2020, underscoring the progress made on inflation. However, it was the core measure which gained most attention as it registered a small beat versus the consensus, rising 0.3% on the month versus an expected 0.2%. The rise in super core inflation is also noteworthy. Prices in core services less housing rose to the highest since April, indicating price pressures are intensifying outside of shelter too. As a result, the odds for a quarter point rate reduction by the Fed next week increased to about 80% from 70% before the release. The probability of a larger 50 basis point cut reduced, but such a move is still not completely off the table.

Although the dollar’s downtrend since June remains intact, the DXY’s 200-week moving average, at 100.4, remains a key support in the short term. Should GBP/USD and EUR/USD break below their psychologically important $1.30 and $1.10 levels respectively, an extended short-term dollar recovery may gain traction ahead of the Fed’s decision next Wednesday.

Pound keeping afloat critical level

George Vessey – Lead FX Strategist

The British pound fell briefly to a 3-week low versus the US dollar yesterday after UK GDP posted no growth in July and US inflation data boosted the dollar. GBP/USD is now down almost 2% from its 2-year high of $1.3266 recorded last month but remains above the key $1.30 handle for now as central bank decisions loom next week.

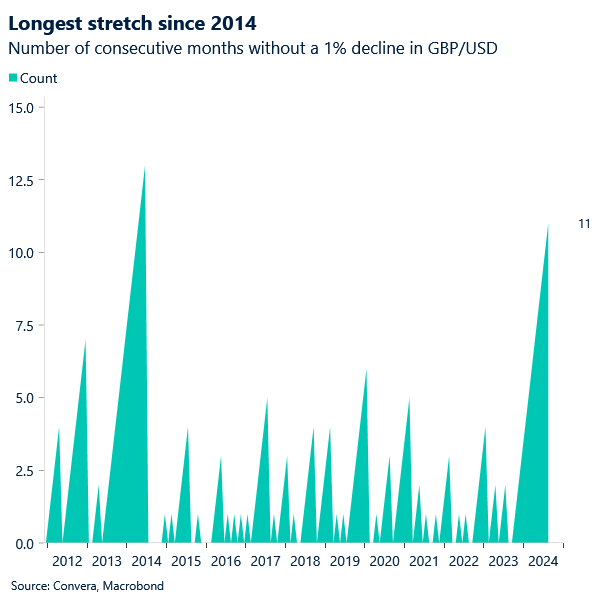

Seasonals don’t look favourable for sterling as September has, on average, been the worst month of the year for GBP/USD since 2000. Currently down 0.6% month-to-date, we could see the pair end what has been the longest period without a 1% monthly decline since 2014. Weighing on the pair has been UK-US rate differentials, which have fallen from 1-year highs lately. This is due to money markets adding to wagers on Bank of England (BoE) easing this year whilst expected Fed easing has fallen slightly in the wake of economic data. However, we still anticipate the BoE will remain the most hawkish among G3 central banks, which should support the pound into year-end.

The next input for these wagers on monetary policy will come from UK inflation data due a day before the BoE decision next Thursday. Any further signs of cooling services inflation could raise BoE easing bets for the remainder of 2024, which currently stands at 50 basis points (two rate cuts). This would be a major headwind for the pound, especially for GBP/USD if the Fed takes a more cautious approach than markets currently anticipate.

Euro softens ahead of the ECB rate decision

Ruta Prieskienyte – Lead FX Strategist

As discussed in yesterday’s update, the euro began Wednesday’s session up by over 0.2% against the US dollar, buoyed by the perceived win of Kamala Harris in the first televised US presidential debate against Trump. However, the common currency later gave up its gains following a hotter-than-expected US core CPI print. This data dashed hopes of a 50bps rate cut by the Fed next week, driving a dollar-positive outcome. In Europe, equities trended lower, reflecting both the spillover effects of disappointing US inflation data and cautious sentiment ahead of the ECB rate decision. Meanwhile, European bonds, particularly German Bunds, continued to see strong demand, with German two-year bond yields falling to their lowest level since March 2023 after seven consecutive sessions of gains.

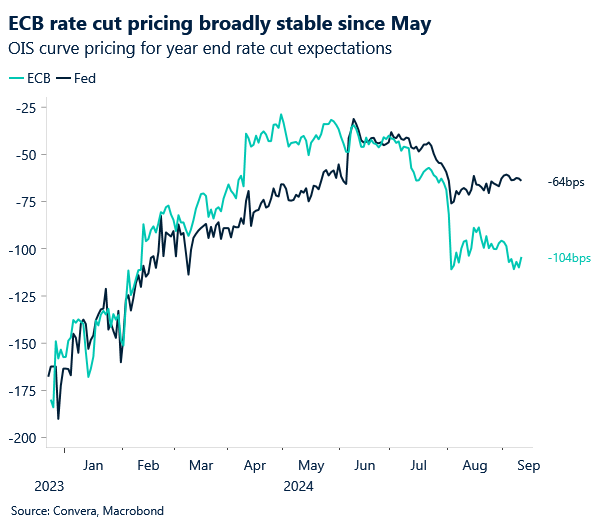

The ECB rate decision later today is the highlight of this week’s domestic calendar, where a 25-basis point cut is widely expected and fully priced in, but the market’s attention will shift to the ECB’s communication and staff forecasts. Signals regarding future rate cuts are unlikely to be firm, as the Governing Council is expected to maintain maximum optionality. We see three main sources of potential euro weakness on the back of today’s decision: (1) Current pricing offers attractive levels for long positions, with only 60bps priced in by year-end. This leaves plentiful room for risk premium, particularly with growth concerns that have yet to be fully acknowledged by the market or equity weakness likely in the coming months. (2) A shift in focus from inflation to growth concerns could accelerate the ECB’s rate-cutting cycle. (3) Given the strong correlations between USD and EUR rates, any dovish comments from ECB President Christine Lagarde could tilt risks toward euro weakness in the near term.

Ahead of the risk event, EUR/USD has moved towards the $1.10 support level, near the 35-day SMA. A break below could see the pair testing the 50-day SMA at $1.096. Additionally, market sentiment, measured by 25-delta risk reversals, has shifted from a bullish to a neutral stance.

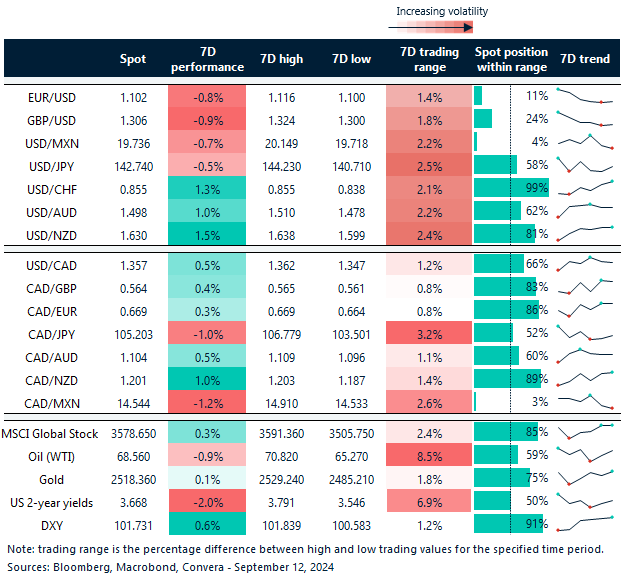

JPY continues to outperform

Table: 7-day currency trends and trading ranges

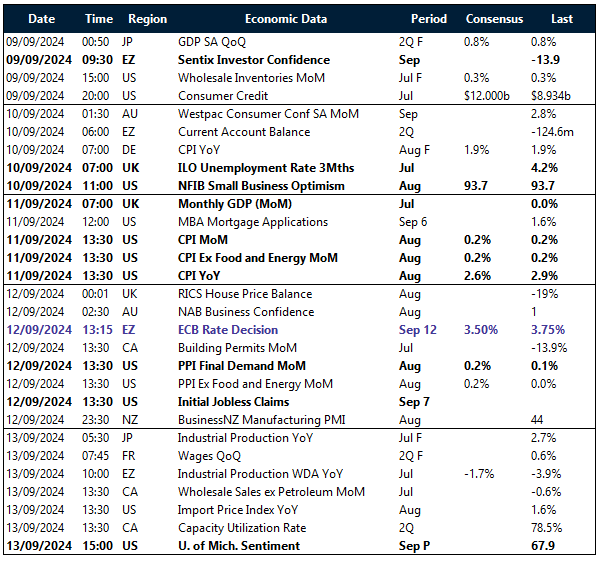

Key global risk events

Calendar: September 9-13

All times are in BST

Have a question? [email protected] *The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.