Written by Convera’s Market Insights team

Pound and gilts dumped

George Vessey – FX Strategist

When bonds fall, yields rise. Typically, when an advanced country’s yields rise, its currency usually rises. This has not been the case in the UK. UK bonds (gilts), the British pound, and UK equity benchmarks all slumped in dramatic fashion yesterday. As bond prices fell, 10-year gilt yields leapt to their highest level since the financial crisis in 2008, while 30-year yields hit their highest since 1998.

The pound dropped more than 1%, with GBP/USD hitting its lowest level in over a year. The pair has fallen through the bottom of its Bollinger band and the break below last year’s low opens up the path toward the October 2023 low at $1.2037. Across the G10 space, sterling experienced unusual volatile (in some cases more than two standard deviations) daily shifts to the downside compared to average daily performances over the past five years. Even GBP/EUR, which has been stable above €1.20 for over a month, is trading nearer €1.19 now.

There was no major catalyst for these moves other than poor demand in the UK’s latest auctions of government debt this week. The cost of long-term borrowing (bond yields) thus soared to fresh multi-decade highs. As reported yesterday, although this dynamic should support the pound through the rates channel, a high-for-longer rate narrative in a weakening economic backdrop may not be all that pound bullish if stagflation (weak growth & sticky inflation) chatter resurfaces. And this was exactly the narrative that resurfaced on Wednesday. The meltdown in UK gilts and the British pound reflects the latest leg in the market’s longer-term reassessment of the UK’s prospects under the Labour government. Those pre-election hopes for a new age of political stability have been substituted by worries over deteriorating confidence, higher taxes, spending and borrowing, little to no growth and sticky inflation.

The pound was therefore at the mercy of these negative headlines, reminiscent of the Liz Truss budget in 2022 back when GBP/USD fell to a record low near $1.03. This time is not as extreme, but the UK’s current and capital account deficit leave it vulnerable to foreign investors who might demand higher yields and a cheaper pound before they’re prepared to buy gilts. The added risk premium towards sterling has disconnected it from the monetary policy path, hence the huge divergence in GBP/USD and UK-US yield spreads over the past few months. It’s certainly eye-catching as the chart below shows.

Unfortunately for the pound, it could be facing a lose-lose situation when it comes to the Bank of England (BoE) and its policy trajectory. The market is currently pricing in barely two cuts from the BoE this year, though sterling has not benefited due to stagflation concerns. Yet, if the BoE sends stronger signals on the need for interest rate cuts, this will also likely weigh on sterling via the yield narrative. For the pound to recover, UK data needs to improve alongside confidence in fiscal policy.

Dollar back on top as jobs report looms

George Vessey – FX Strategist

The US dollar is back on the offensive after more upbeat economic data and hawkish minutes from the December policy-making meeting of the Fed. Both have justified the aggressive response to the pivot toward a more hawkish stance of future rate cuts and the dollar’s rebound against major peers. That said, most of the good news is priced into the dollar and Treasuries, with long-term bond yields approaching 5%.

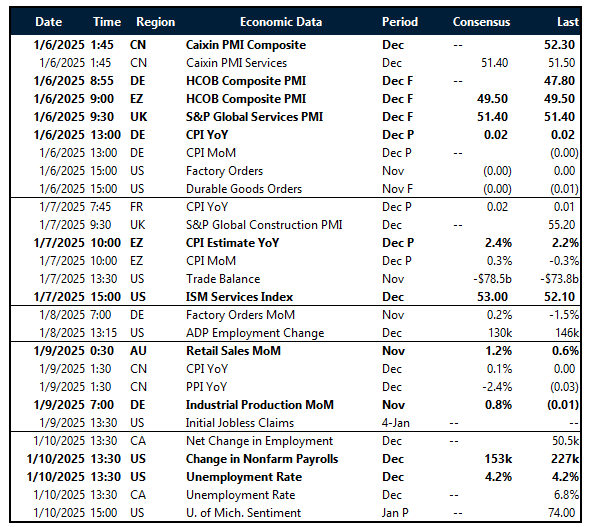

Investors are now focused on Friday’s monthly jobs report, one of the last major data releases before the Fed’s upcoming monetary policy decision. It will be the final monthly labour market figures before officials head into a blackout period. The consensus forecast is for payrolls in the US to have risen 163,000, the jobless rate probably held steady at 4.2%, while average hourly earnings are projected to have risen 0.3% from a month earlier. Our chart below shows why inflation and jobs data attract so much attention. The market’s pricing of the Fed funds rate has nearly perfectly followed the surprise index for inflation and the labour market, showing that the dual mandate continues to dictate markets perception of policy makers.

The month of October was both the turning point for this proxy indicator for the Fed’s dual mandate and the US dollar. However, while the index stagnated since November, the Greenback continued to power on due to 1) the Trump trade and 2) political risks outside of the US starting to build.

No reprise for the euro

Boris Kovacevic – Global Macro Strategist

The EUR/USD has experienced a volatile day yesterday and is trading around $1.03 this morning. This week, the US dollar has been supported by a series of strong US economic data releases, including robust employment figures and positive consumer confidence. These data points have reinforced expectations of a continued hawkish stance from the Fed, bolstering the greenback.

Conversely, the Euro has been weighed down by weak economic data emanating from the Eurozone. Notably, German factory orders declined unexpectedly in November, signaling deeper economic challenges for the region. Furthermore, German retail sales also contracted in November, adding to concerns about the health of the Eurozone’s largest economy. This combination of disappointing data, coupled with concerns about the ongoing energy crisis (rising gas prices), has dampened investor sentiment and put further pressure on the Euro.

The near-term outlook for the EUR/USD remains uncertain. Continued strong US economic data and a hawkish Fed could further pressure the common currency. However, any signs of weakness in the US economy or a more dovish shift from the Fed could provide some support for the euro.

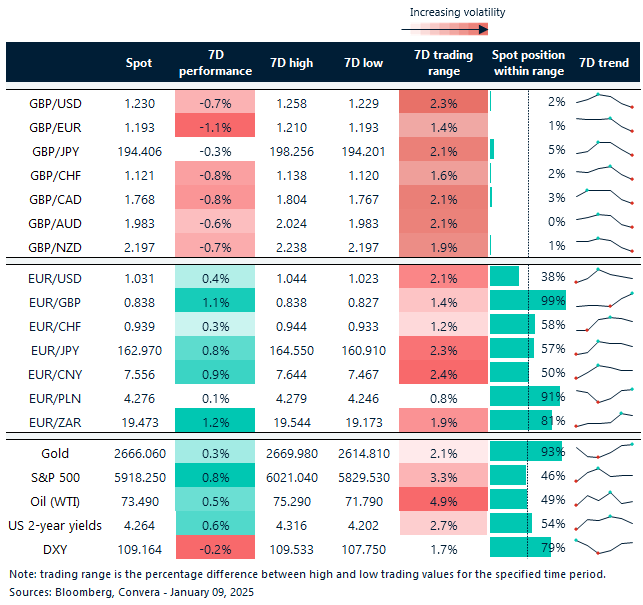

Pound absolutely clobbered across the board

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: January 6-10

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.